Financier №4 (40) 2025

Rational Investments

Freedom analysts suggest buying shares of the most promising players in the telecom industry

Upside potential and quotes are as of December 1

Mikhail Denislamov,

Deputy Director of the Analytical Department at Freedom Finance Global

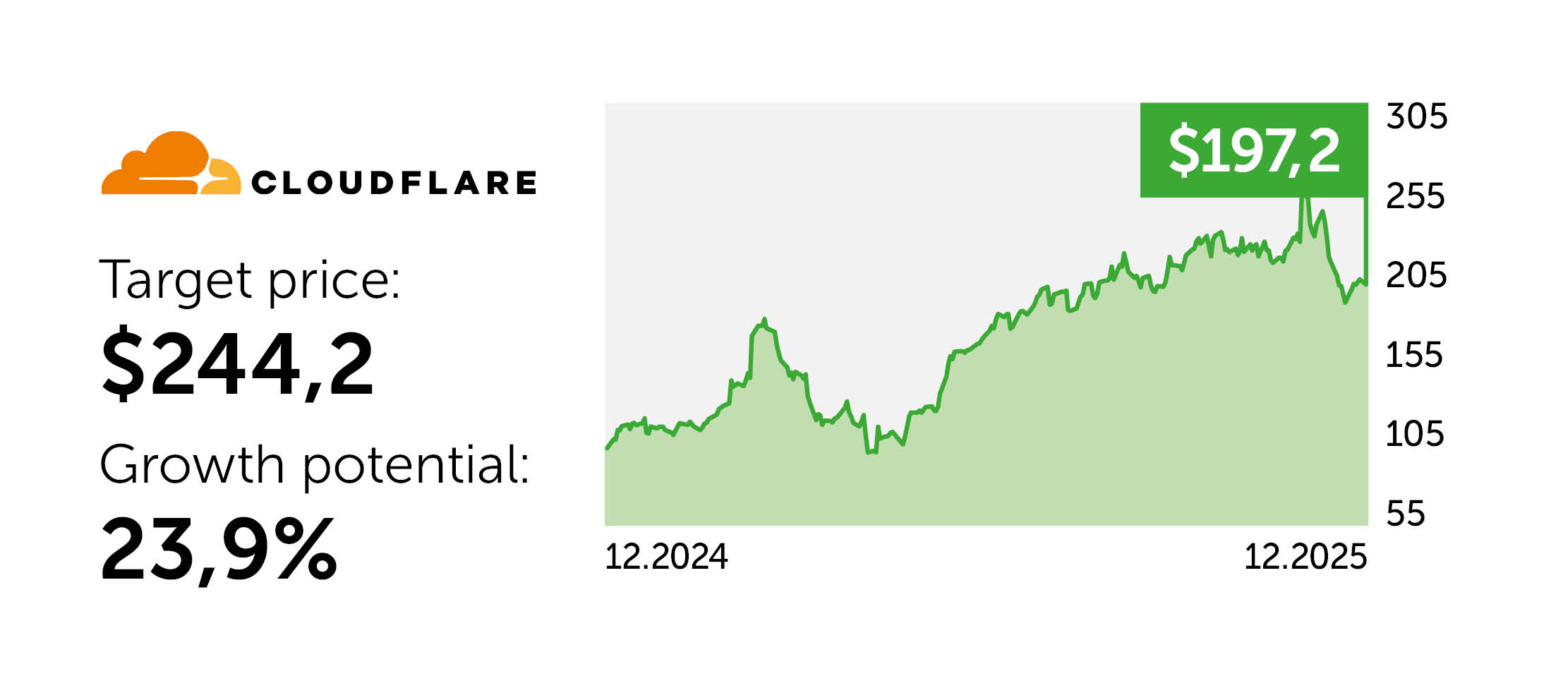

Cloudflare (NET) provides cloud networking and cybersecurity solutions that accelerate data transfer, including AI traffic, while providing reliable protection. The consensus forecast for 2026 projects Cloudflare revenue growth of 27% YoY to $2.7 billion, driven by platform scaling and the strengthening of its position in the security segment. Share price growth is driven by an expanding base of large enterprise customers, active cross-selling of security modules, and a potential upward revision of forecasts. NET shares are attractive to long-term investors betting on increased demand for cloud security and edge solutions.

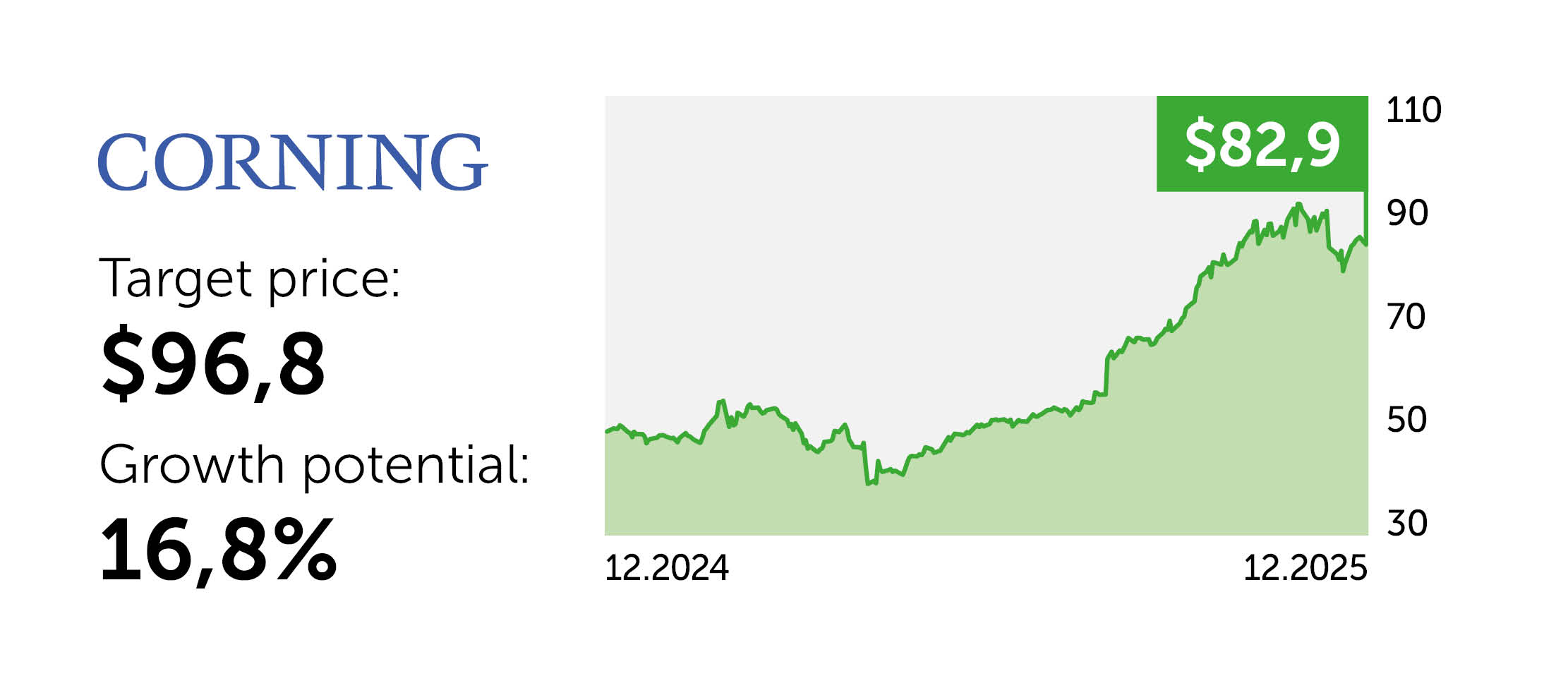

Corning (GLW) is a global leader in the development of specialized materials for technology industries. The company’s primary revenue driver is the rapid expansion of AI infrastructure. High demand for optical connections for data centers and internet backbones will drive sales of optical solutions (the company’s largest and highest-margin business segment) to increase by more than 20%. Corning’s product shortages, limited capacity growth, the rising share of high-margin products in its sales mix, and share buybacks create favorable conditions for earnings per share growth of around 20% annually.

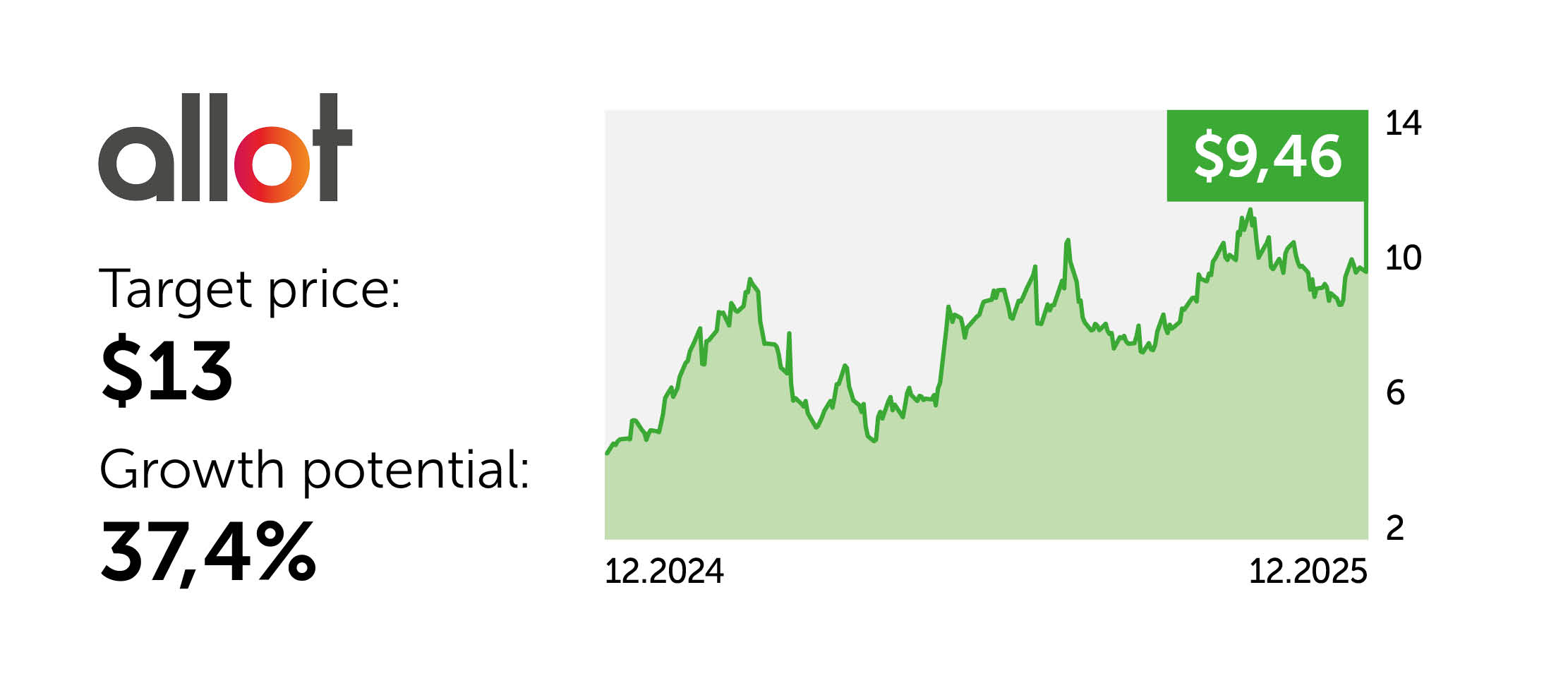

Allot (ALLT) offers network analytics and cybersecurity tools to telecom operators worldwide. The company has returned to double-digit revenue growth and posted its best operating profit in a decade, driven by strong performance in its Security-as-a-Service (SECaaS) segment. Key positive drivers for Allot include the transition to a high-margin, recurring revenue model through SECaaS, the successful launch of its services by major clients such as Verizon and Vodafone, and the signing of multimillion-dollar contracts. Long-term revenue growth will support the company’s stock price movement toward its target.

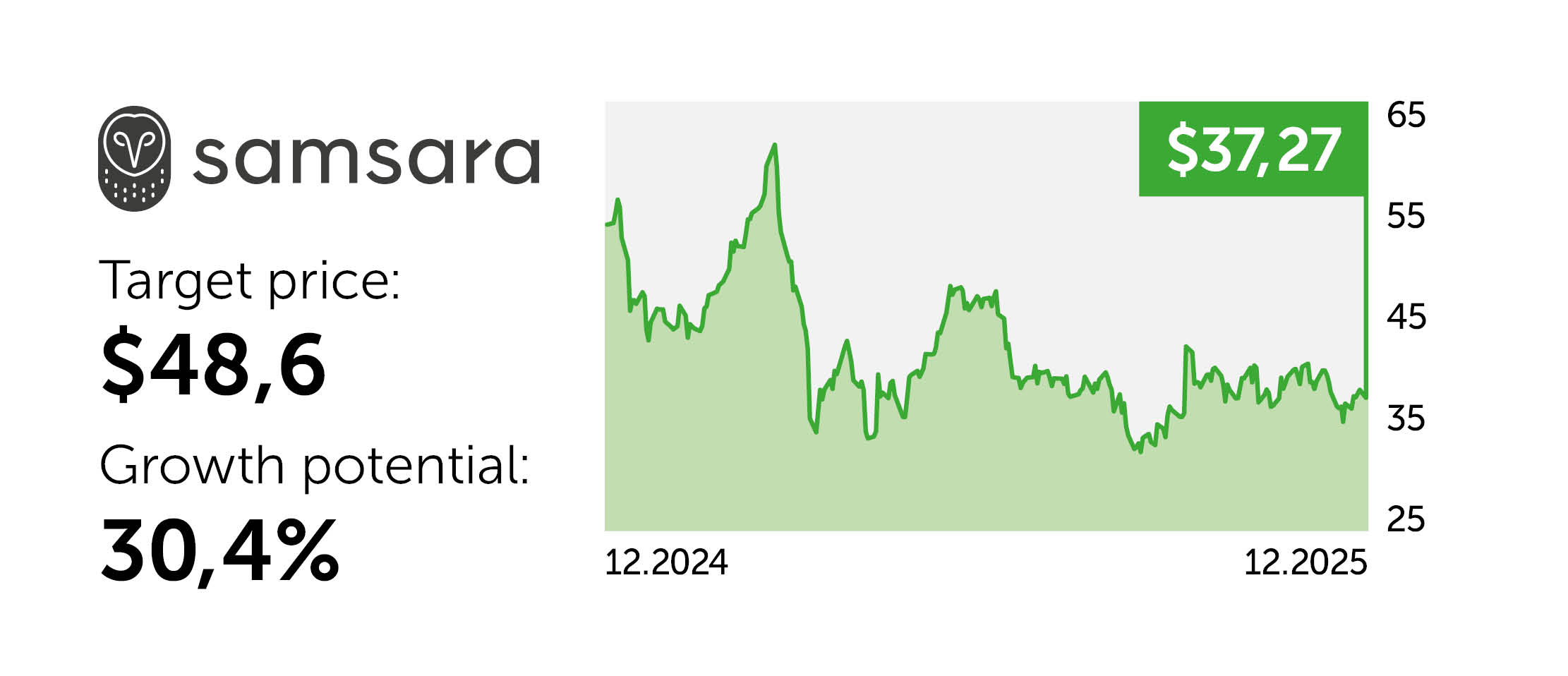

Samsara (IOT) is a provider of a Connected Operations Cloud platform that integrates sensors, video cameras, and telematics for fleets, logistics, and industrial operations. Using the company’s edge analytics and AI solutions, accidents, fuel consumption, and equipment downtime are reduced. With EPS growth of 20–30% expected over the next two years and an expanding base of connected assets as physical operations become increasingly digitized, Samsara represents an investment opportunity at the intersection of IoT*, communications, and new technologies for the logistics sector. A positive driver for the company’s shares is the rollout of new AI modules, which are expected to improve business margins.

*Internet of Things

Yerlan Abdikarimov,

Director of the Financial Analysis Department at Freedom Broker

T-Mobile (TMUS) has raised its annual forecast while maintaining double-digit profit growth. High free cash flow (FCF) and the buyback ensure a comfortable 16% dividend increase, despite earnings pressure related to the integration of U.S. Cellular. The debt burden remains under control, and liquidity levels allow continued investment in growth. The current correction offers an attractive entry point for positions based on a combination of share price appreciation and stable dividend growth. Risks include increased competition amid declining consumer activity due to high interest rates.

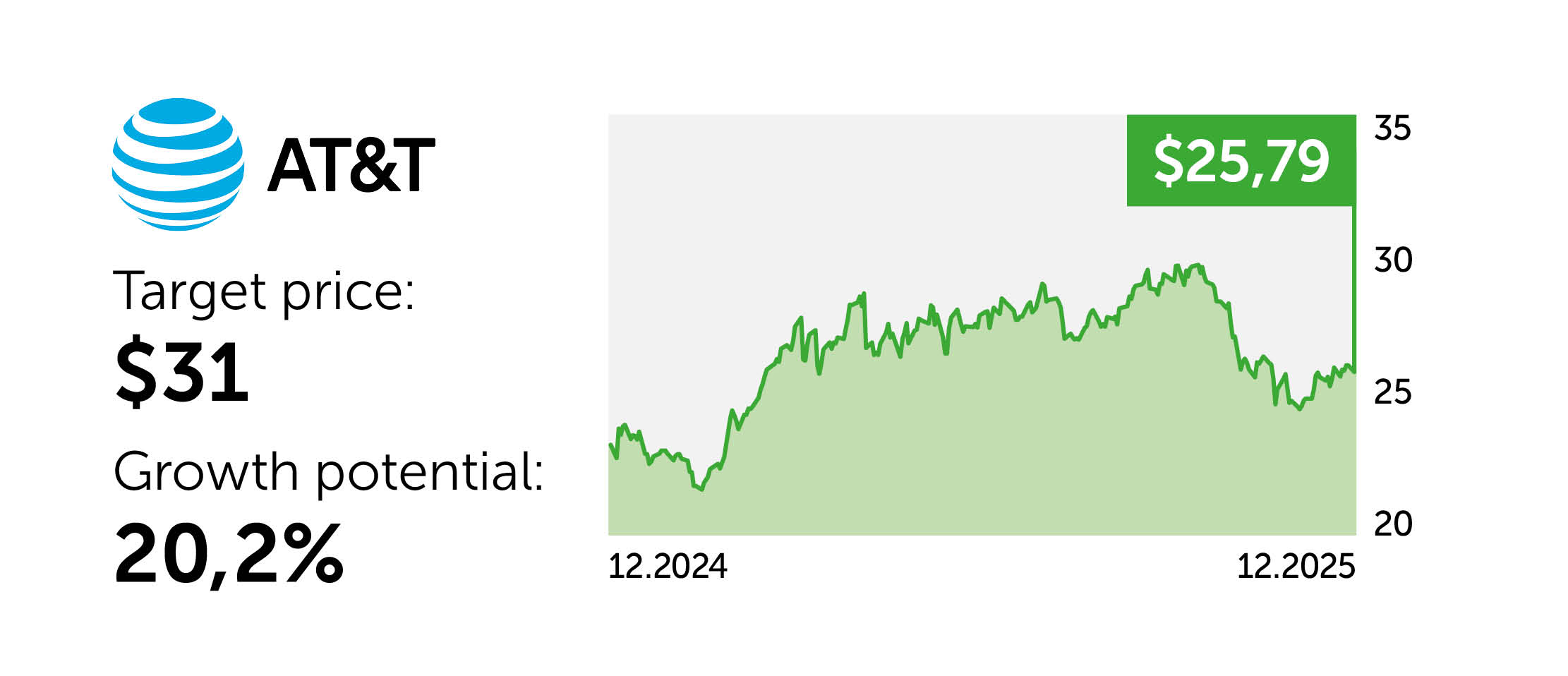

AT&T (T) has confirmed its free cash flow forecast at $16 billion, paving the way for dividend increases and continued buybacks. The 2025 buyback program has been approved at $4 billion, providing a rare yield of 2.58% for the sector. The Net Debt/EBITDA ratio is approaching the company’s target level. Significant investments in 5G and fiber-optic infrastructure development increase the issuer’s attractiveness as a buy. Strong cash flow, a prudent profit distribution policy, and a strengthening balance sheet create a favorable risk profile, supporting share price growth and a return to regular dividend increases.

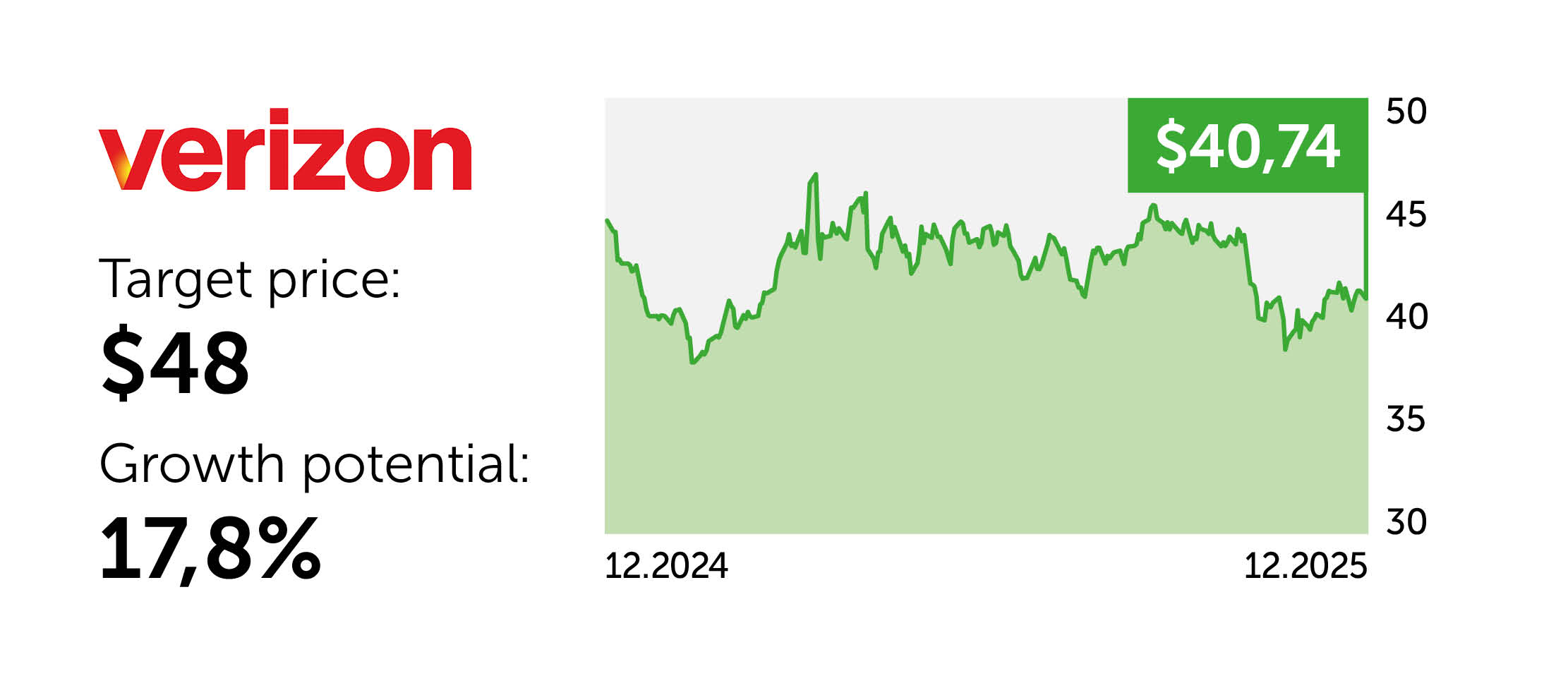

Verizon Communications (VZ) attracts investors with an impressive 6.7% dividend yield and high FCF. The new management’s priority is improving margins. In Q3, the company demonstrated solid revenue growth, cost efficiency, and margin expansion. The issuer’s P/E multiple is in the range of 5–7. VZ shares are an attractive purchase in a declining interest rate environment, as they offer the opportunity to generate stable income. The shares’ fair value will be reassessed as strategic initiatives are implemented, the user base expands, and operating expenses are optimized.

América Móvil (AMX) combines scale, high profitability, and a strong position in Latin America. In Q3, revenue, EBITDA, and FCF (+47% YoY) outperformed the sector as a whole. The potential acquisition of Telefónica Chile’s assets, together with Entel, could accelerate the company’s regional expansion and increase operating synergies. A Net Debt/EBITDA ratio of 1.55x, as well as EV/EBITDA and forward P/E multiples, indicate that the stock is undervalued relative to peers. Its attractiveness is further supported by the combination of defensive characteristics and the issuer’s potential for sustainable growth in Latin America.