Financier №4 (40) 2025

Saltanat Ilyasova

senior personal manager, Freedom Broker

Working at the Edge of the Internet

What Has Changed in Telecoms with the Advent of Artificial Intelligence

The traditional way of searching the internet—entering a query into a search engine and receiving a list of links in a fraction of a second—is gradually becoming obsolete. Increasingly, users are delegating research, analysis, and ready-made answers to AI services integrated directly into browsers and applications. This convenience, however, comes at a significant cost.

Energy Surge

Processing a standard Google search query consumes around 0.3 Wh of electricity—enough to power a 60-watt light bulb for approximately 17 seconds. By contrast, generating a single response using ChatGPT-5 requires about 18 Wh. With approximately 2.5 billion queries processed daily, this AI assistant consumes roughly 45 GWh of electricity per day—equivalent to the daily consumption of around 1.5 million US households.

In 2024, Huawei estimated that the total volume of data generated globally had reached 80 zettabytes*. By 2030, this figure is expected to increase by a factor of 12.5.

*A zettabyte equals one trillion gigabytes.

Energy consumption, however, is only part of the challenge. Training large language models requires the simultaneous transfer of petabytes of data between hundreds of servers. According to analytics firm Omdia, data centre-to-data centre traffic generated by AI workloads is expected to more than double annually over the next five years.

Speed and reliability are critical. With the development of so-called physical AI—including autonomous vehicles and robotic factories—response time becomes a decisive factor. Sending data to a central cloud and back typically takes 50–100 milliseconds, making many real-time AI applications unfeasible.

For an autonomous vehicle traveling at 100 km/h, a 100-millisecond delay means the car will travel nearly 2.8 meters before a decision is executed. In practice, this could mean that the vehicle reacts to a suddenly appearing obstacle too late, significantly increasing the risk of accidents.

Edge Computing—the processing of data as close as possible to its source—offers a solution to these challenges while also reducing energy consumption and bandwidth requirements. By shifting computation away from centralized cloud data centers and towards local infrastructure, edge computing reduces network load, improves service reliability, and enables real-time decision-making. This approach is a prerequisite for the mass adoption of self-driving vehicles and other latency-sensitive technologies.

At the Edge of the Network

Imagine needing to multiply two large numbers, but instead of using a calculator, you ask a mathematician located hundreds of kilometers away. Traditional cloud computing operates on a similar principle. Edge computing fundamentally changes this model by placing processing power where data is generated—within the user’s immediate digital environment. Distributed computing moves data processing and storage closer to the source, relying on local data centers, network nodes, and even end devices themselves. This results in faster access to information, near-instant responses, enhanced privacy, and more efficient resource use.

These advantages—rare for infrastructure projects—create attractive opportunities for investors, even at early stages of deployment. While public attention is focused on applications such as ChatGPT, much of the value is being generated by those building the underlying infrastructure: chip manufacturers, network equipment suppliers, data centre operators, and telecom companies.

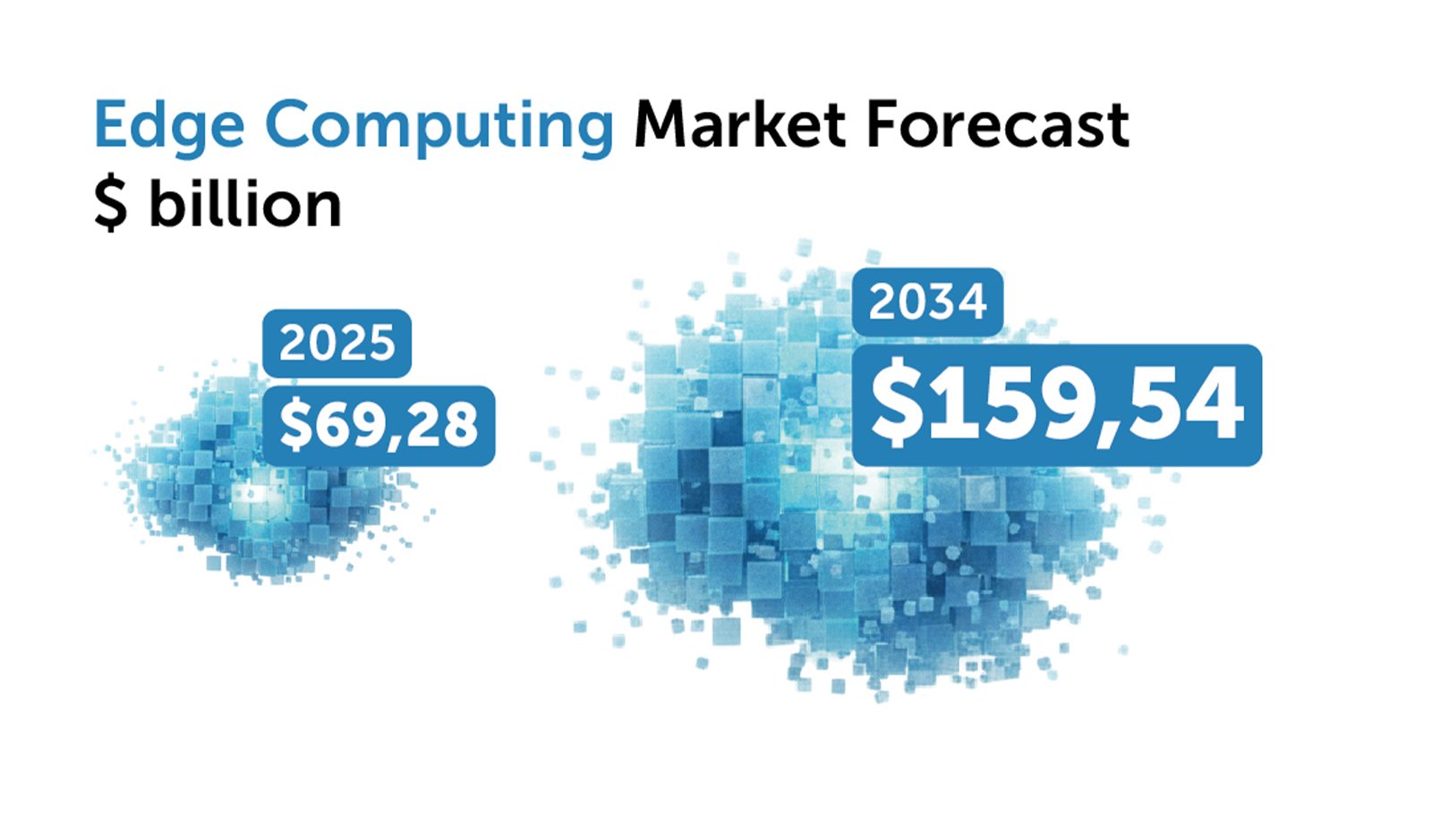

Source: precedenceresearch.com

Wired Momentum

Everything outside large centralized cloud and corporate data centers forms the edge of the network. Examining the data creation and processing chain reveals the key beneficiaries at each level.

Level 1. Hardware

The first layer of the edge computing ecosystem consists of end devices—not only smartphones and personal computers, but also autonomous vehicles, industrial machinery, and Internet of Things (IoT) equipment. Companies are increasingly seeking to make these devices more autonomous and less dependent on external servers, driving demand for high-performance chips and sensors. NVIDIA (NVDA) remains the undisputed leader in this segment, supplying advanced processors for PCs, workstations, autonomous vehicles, and robotics. AMD (AMD) is a key competitor in PC hardware, while Qualcomm (QCOM) focuses primarily on smartphone chips and has been steadily expanding into IoT and automotive solutions. Other major beneficiaries include Intel (INTC), Texas Instruments (TXN), Analog Devices (ADI), and Micron Technology (MU), whose products enable a significant share of computation and data storage to take place close to the point of data generation.

Level 2. Edge Services

Edge gateways act as intelligent intermediaries between devices and edge servers, aggregating and pre-processing data from multiple sources. These are not consumer-grade Wi-Fi routers, but complex enterprise and industrial systems with advanced data management capabilities. Cisco Systems (CSCO) remains the dominant player in this segment, with Juniper Networks (JNPR) also holding a strong position. Other participants include industrial conglomerates Siemens and Schneider Electric, as well as specialized firms such as F5 Networks, Advantech, Rockwell Automation (ROK), Digi International (DGII), and Palo Alto Networks (PANW), which focuses on cybersecurity solutions.

Level 3. Data in Motion

Once collected, data is transmitted to local edge servers (edge nodes), where advanced analytics, model training, and AI inference are performed. This is where the main competitive battle for the edge computing market is unfolding.

Key players include server manufacturers, telecommunications operators, digital infrastructure companies, and content delivery network (CDN) providers that accelerate data transmission to end users.

Dell Technologies (DELL) remains the largest participant in this segment, benefiting from rapid growth in AI server shipments. For the first time in the company’s history, its data centre business surpassed its personal computer division in 2025. Hewlett Packard Enterprise (HPE) is also benefiting from the AI boom, with both companies actively expanding their edge computing offerings.

Data transmission to local servers is dominated by companies such as Equinix (EQIX), the world’s largest data centre operator, along with competitors Digital Realty Trust (DLR) and Crown Castle (CCI). Traditional telecom operators are emerging as new leaders in edge computing. Verizon (VZ), AT&T (T), and T-Mobile (TMUS) have been developing edge-focused services for several years. For these companies, expanding AI-ready infrastructure could become a new revenue stream capable of reversing long-term stagnation in average revenue per user.

CDN providers also stand to benefit. Cloudflare (NET) and Akamai Technologies (AKAM) operate global networks of distributed servers that accelerate content delivery regardless of user location. Amazon (AMZN) and Alphabet (GOOGL) offer similar services, although CDNs represent only one component of their broader cloud ecosystems.

Nexus

The growth of edge servers and rising data volumes are driving demand for ultra-fast connections between major network nodes. As noted earlier, AI-related traffic between data centers is expected to more than double annually over the next five years.To meet this demand, operators are rapidly upgrading backbone networks, leading to double-digit growth in orders for optical fibre and related equipment.

Corning (GLW), the world’s largest fibre-optic manufacturer, has emerged as a key beneficiary. The company recently announced that it has reserved 10% of its global fibre production capacity for the next two years specifically for AI data centre connectivity. Other major fibre producers—including Prysmian Group, Sumitomo Electric, and Furukawa—are also well positioned to benefit from this trend.

The integration of artificial intelligence into communications infrastructure, and the resulting expansion of edge computing, represents a fundamental transformation of the digital ecosystem. For investors, the need for greater network capacity has become a powerful new driver of capital growth.