Investment Review №342. A Delicate Balance

An Attempt at a Comeback

Signs of de-escalation in the Middle East contributed to a rebound in local markets

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

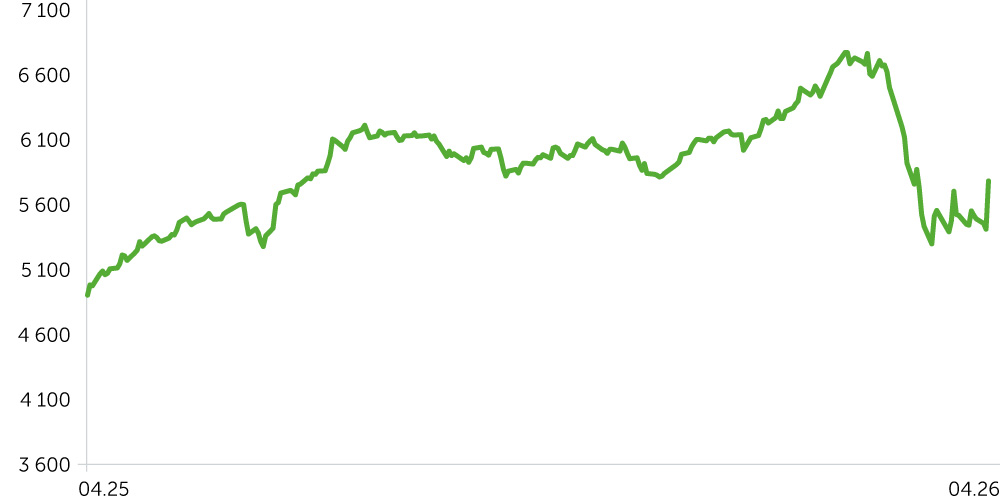

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

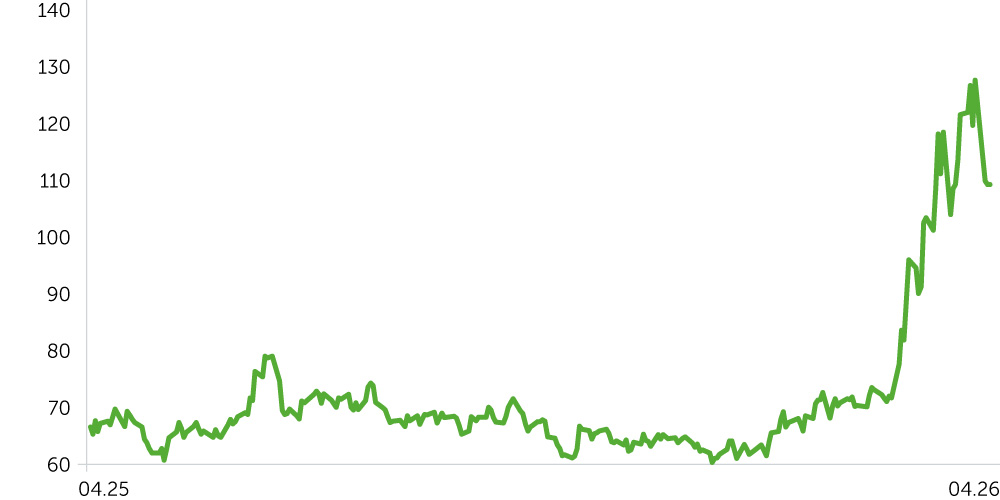

Brent Oil, 1-Year Dynamics

Between March 23 and April 6, 2026, UAE equities recovered gradually, supported by a moderate easing of geopolitical tensions and early signals of a potential U.S.–Iran ceasefire. The Dubai Financial Market (DFM) Index rose 1.2%, reaching 5,448 from 5,383, while the Abu Dhabi Securities Exchange (ADX) Index gained 2.1%, climbing to 9,625 from 9,423. This outperformance contrasts with the 0.5% rise in the S&P 500, reflecting regional resilience amid partially narrowing risk premia. Meanwhile, Brent crude surged 5.8% to $110 from $104/bbl, boosted by the April 7 U.S.–Iran two-week conditional ceasefire and the immediate reopening of the Strait of Hormuz. The development drove significant market reactions on April 8, with the DFM jumping 6.9% and the ADX rising 2.8%.

Over the past two weeks, sectoral performance has been broadly positive, led by Communication Services, Financials, and Real Estate.

Communication Services led gains, posting average returns of +4.12%, driven by Sudatel (SDTL) up 7.03%, du (EITC) up 4.39%, and e& (ETISALAT) up 4.03%. Financials climbed roughly 2.5% on average, led by Emirates NBD (+7.86%), Abu Dhabi Islamic Bank (+7.51%), First Abu Dhabi Bank (+6.36%), and Abu Dhabi Commercial Bank (+5.92%).

Real Estate saw a moderate recovery, averaging +1.34%, with Aldar Properties leading the sector at +7.89%. Consumer staples lagged, declining 7.25% amid constrained demand and elevated fuel-driven inflation, led by Spinneys (−9.63%) and Agthia Group (−3.80%).

The yield on UAE proxy Treasury bonds rose 35.3bps, from 4.89% to 5.25%, while U.S. Treasury yields declined from 4.48% to 4.39% (−9 bps) over the same period. Consequently, the spread between UAE proxy bonds and U.S. Treasuries widened from 41 to 86 bps. This widening spread, coupled with falling U.S. yields, highlights sustained pressure on UAE assets as relatively riskier regional instruments. Investors demanded higher compensation amid uncertainty surrounding the military conflict, whereas the drop in U.S. yields signals continued strong demand under a flight-to-quality strategy.

Economic Updates

- GDP proxy and business activity: UAE maintains growth despite regional tensions. The S&P Global UAE PMI fell to 52.9 in March from 55.0 in February, remaining above the 50 mark that signals ongoing economic expansion. The slowdown reflected weaker consumer demand, supply chain disruptions, and a sharp rise in input prices—the largest increase since July 2024. Business sentiment slipped to a 61-month low, yet companies remain optimistic, supported by sustained long-term demand in the IT sector and fiscal measures under the Abu Dhabi Economic Vision 2030.

- Dubai unveiled a Dh1bn (>$270m) stimulus package. On March 29, Sheikh Hamdan bin Mohammed—Crown Prince of Dubai—approved a Dh1bn ($272m) stimulus package, effective April 1, 2026, for 3–6 months. The five-component program offers three-month deferrals of select government fees, hotel and tourism levy postponements, an extension of the customs grace period from 30 to 90 days, and streamlined residency procedures, targeting sectors most affected, notably tourism and hospitality.

- Inflationary pressure: fuel prices and secondary effects. Fuel prices in the UAE surged sharply in April, with diesel rising over 70% and gasoline (Special 95) up more than 30%. According to S&P Global Market Intelligence, this increase contributed roughly +1.3 percentage points to consumer inflation, with additional secondary effects stemming from higher transportation and logistics costs. Despite these pressures, analysts expect annual inflation to remain moderate at 1.8–2.0%, supported by the UAE economy’s structural flexibility.

- The UAE entered the top-10 global exporters for the first time. Total merchandise trade hit $1.637tn in 2025, with non-oil exports surging 45% to ~$221bn and the trade surplus reaching a record ~$159bn.

- Dubai real estate shows early signs of stabilization. For 1Q26, 47,996 transactions were recorded, totaling ~$48.1bn, with March volumes up 5.5% YoY in deal count and 23.4% YoY in value. Off-plan transactions accounted for 70% of activity. Early March, Goldman Sachs reported a 37% YoY drop in volumes, characterizing it as a “liquidity freeze” rather than a structural collapse. On April 2, Fitch flagged potential deterioration in bank asset quality, concentrated in the Real Estate sector.

Corporate News

- e& / Emirates Telecommunications Group (ADX: EAND) rose 4.03% over the two-week period. In March, e& and Khalifa University published a technical paper on 6G network architecture with native AI integration.

- Aldar Properties (ADX: ALDAR) gained 7.89% over the period. March operational update confirms business resilience. Construction continues across all 141 active sites in Abu Dhabi, Dubai, and Ras Al Khaimah, with 1,075 housing units completed YTD, including 550 in March. YTD construction contracts total ~$1.28bn, ~$490m of which was awarded to five contractors in March; active tender pipeline exceeds ~$8.2bn.

- Masdar and TotalEnergies launched a renewable energy JV in Asia. On April 2, Masdar and TotalEnergies signed a $2.2bn 50/50 JV to consolidate onshore renewable assets across nine Asian markets. Platform includes 3GW of operational capacity and 6GW in active development across Azerbaijan, Indonesia, Japan, Kazakhstan, Malaysia, Philippines, Singapore, South Korea, and Uzbekistan.

Two-Week Outlook

The key inflection point struck April 7, when authorities announced a temporary U.S.–Iran ceasefire and reopened the Strait of Hormuz. Markets surged: DFM jumped 6.9%, ADX climbed 2.8%, Emaar Properties soared 13%, ADIB rallied 10.5%, and Aldar Properties advanced 10%. The truce remains conditional and two-week in duration, with its outcome set to dictate near-term market direction. Over the next fortnight, investors will track final settlement negotiations, gauge oil price reactions to OPEC+’s +206kb/d production hike from May 2026 and assess early April real estate transaction data.

The oil market entered April with mixed factors. WTI rose 11.9% in the week ending April 6, reaching $111.5 per barrel, with the entire gain occurring on Thursday, April 3, amid expectations of a U.S. ground military operation in Iran. At the April 5 OPEC+ meeting, eight countries—Saudi Arabia, Russia, UAE, Iraq, Kuwait, Kazakhstan, Algeria, and Oman—voted to lift May production quotas by +206k bpd. Medium- and long-term fundamentals point to downward price pressure: the Strait of Hormuz reopening and gradual OPEC+ supply increases are expected to weigh on benchmarks. Short-term dynamics, however, remain dictated by the progress of U.S.–Iran negotiations.

Under the base case, the ceasefire evolves into a more durable agreement: the Strait of Hormuz remains open, oil prices adjust down from ~$110/bbl, and the UAE risk premium gradually contracts. The UAE banking sector emerges as the primary beneficiary: a 17% capital adequacy ratio and >146.6% liquidity coverage provide a substantial buffer. Total banking system assets exceed Dh5.42tn ($1.48tn), with the UAE Central Bank’s support package offering additional shock protection. Defensive sectors—Communication Services, Consumer Staples, and diversified financial holdings—are likely to continue showing relative resilience.

In a downside case, a ceasefire breakdown or renewed Strait of Hormuz blockade could trigger a market pullback. Developers with high leverage, banks concentrated in real estate lending, as well as the aviation and logistics sectors would remain most exposed. The essential Consumer Staples sector would continue to face structural pressure from elevated fuel and transportation costs.