Investment Review №342. A Delicate Balance

Inflation Has Roused the “Bears”

Growth Momentum Persists Even as Inflationary Pressures Firm

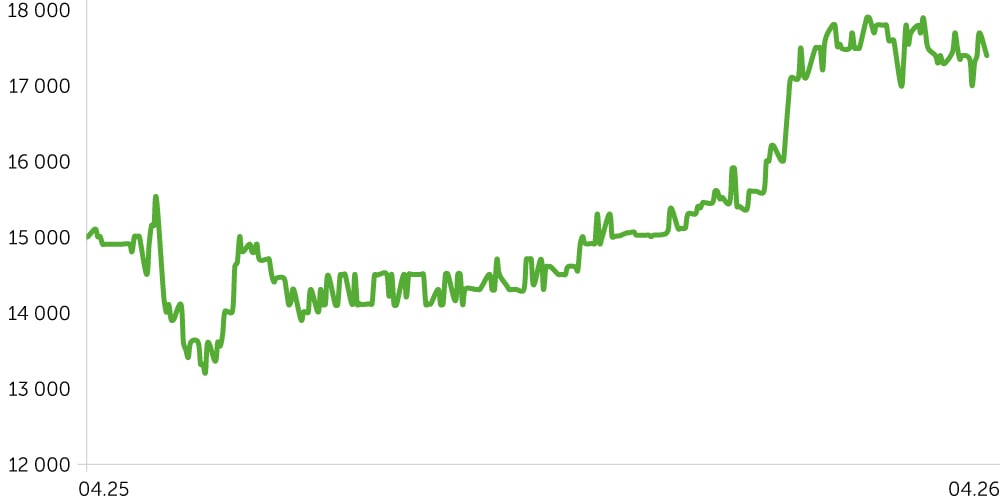

Telecom Armenia Stock Performance (Post-IPO)

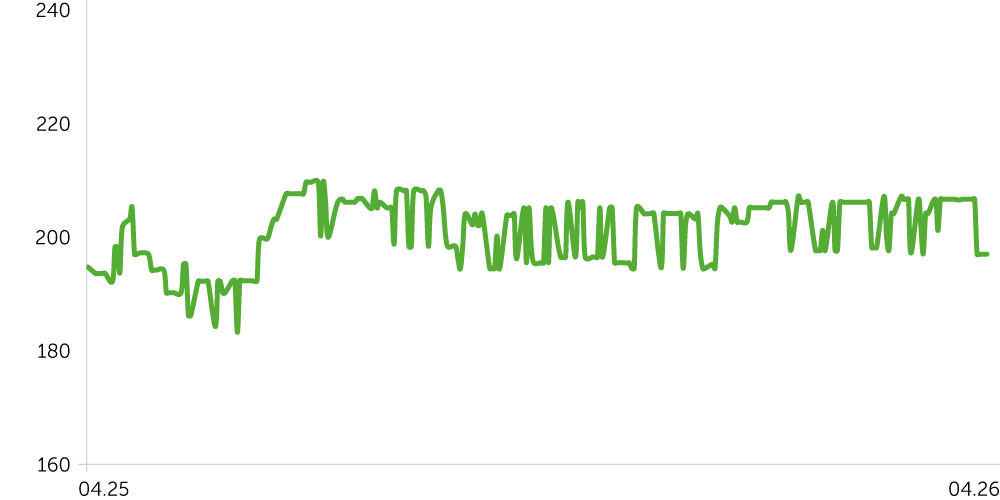

ACBA Bank: 1-Year Stock Trends

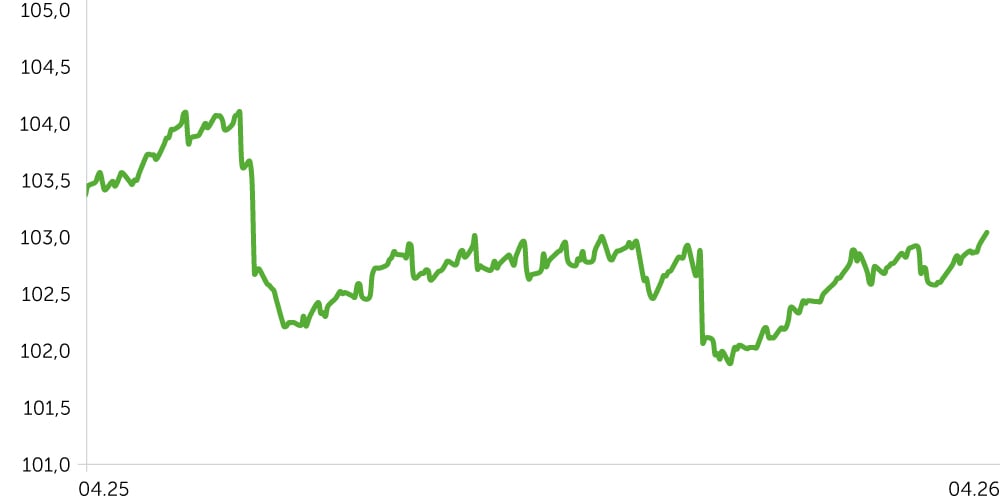

USD/AMD: 1-Year Dynamics

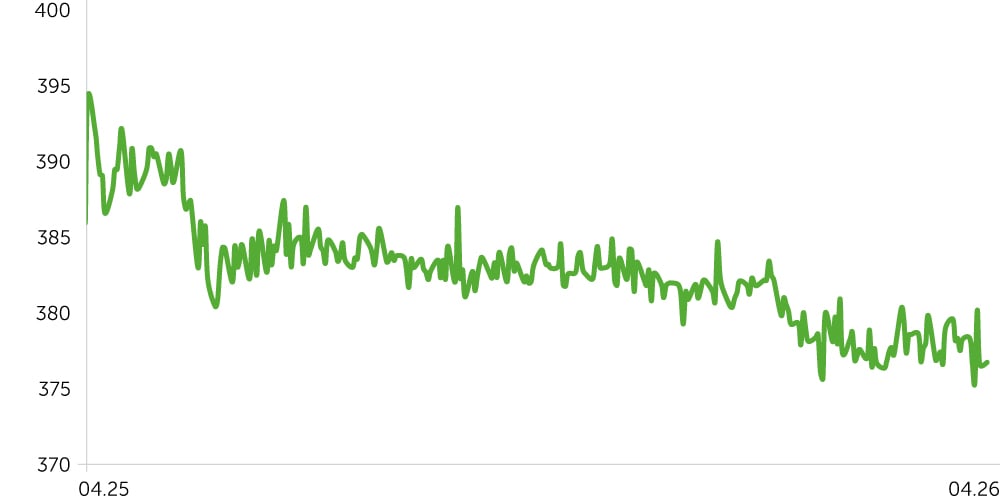

3-Year Corporate Bond Index (AMD) – Post-Update

From March 23 to April 6, 2026, Armenia’s equity market was mixed amid persistent inflation risks and economic activity that came in slightly below market expectations, even as foreign trade posted strong February growth. Telecom Armenia (AMTL) declined 4.7%, while Acba Bank (ACBA) edged down 0.3%. Year to date, however, ACBA is up 11.5%, suggesting continued investor interest in the Financial sector. Economic activity rose 7.2% YoY in February, albeit below expectations, while outperformance in industry and construction provides a positive backdrop for the local market.

The 3-year AMD corporate bond price index rose 0.3%, indicating steady demand for local debt even as inflation remains above the central bank’s target range. Inflation accelerated to 4.5% YoY in March, and producer prices were up 9.5% YoY in February, underscoring ongoing cost pressures. This macro backdrop—together with persistent external pro-inflationary risks, if sustained—could prompt the regulator to adopt a more hawkish tone in the near term. Specifically, a potential partial closure or disruption of the Strait of Hormuz would elevate imported inflation risks by keeping oil prices around $90 per barrel.

That said, the dram remained relatively resilient, appreciating a further 0.8% against the U.S. dollar over the period and helping to cushion imported inflation.

Economic Updates

Between March 23 and April 6, 2026, Armenia’s macroeconomic data indicated continued solid growth in economic activity and a revival in foreign trade, alongside a further build-up of inflationary pressures. On the positive side, the composition of growth appears broadly healthy. However, the persistence of inflation above the Central Bank of Armenia’s target, together with elevated PPI readings, increases the weight the regulator is likely to place on price dynamics in its near-term policy decisions.

- Armenia’s foreign trade rebounded sharply in February, up 30.8% YoY and 37.1% MoM, signaling a marked pickup in cross-border activity after last year’s weak start. Following January’s contraction, exports recovered (+37.6% YoY, +44.2% MoM), outpacing imports (+26.9% YoY, +32.9% MoM). That said, the trade deficit remains wide, underscoring the economy’s structural reliance on imports. The strength and volatility in February likely reflect low-base effects and the normalization of some commodity flows; data from the coming months will be needed to confirm a durable trend.

- Consumer inflation reached 4.5% YoY in March (+0.7% MoM), slightly below the 4.7% YoY market consensus but firmly above the Central Bank’s target band of 3% ±1 pp. Food prices remain the key driver, rising 7.8% YoY (+1.8% MoM), while non-food inflation remains moderate at 0.8% YoY. With producer prices up 9.5% YoY in February, the March data corroborates ongoing cost pass-through to final prices.

- Economic activity increased by 7.2% YoY and 4.5% MoM in February—a bit below market expectations. While the print came in below the 8.3% YoY consensus, the data still indicated solid macroeconomic momentum early in the year. Industry (+23.8% YoY) and construction (+21.8% YoY) remained key drivers. The growth mix appears solid, supported by broad-based gains in industrial and construction activity. However, a 1.7% MoM decline in services points to uneven dynamics across sectors, and the durability of the current industrial upswing will need confirmation in subsequent periods.

Corporate News

- AMIO Bank has announced a public offering of 2-year AMD bonds with a 10% annual coupon, payable quarterly, in an aggregate principal amount of AMD 2.5bn. The offering completion is on June 10, 2026.

Two-Week Outlook

Between April 10 and 20, no major macroeconomic releases are scheduled. As a result, market attention is likely to focus on reassessing recently published data and refining expectations for the Central Bank’s policy path.

During this relatively quiet window, March inflation is likely to remain the key driver for debt market. An acceleration in CPI, together with February’s sharp rise in producer prices, increases the likelihood that the Central Bank will maintain a wait‑and‑see stance—or even adopt a slightly more hawkish tone—in the near term. In our base case, the lack of fresh, convincing disinflation signals, coupled with persistent external pro‑inflationary pressures, points to potentially tougher policy rhetoric from the Central Bank. Meanwhile, the local yield curve is likely to continue to embed an elevated inflation risk premium.