Investment Review №341. The Obvious and the Unbelievable

High-Pressure Area

The military operation against Iran continues to trigger sell-offs on the UAE stock exchanges

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

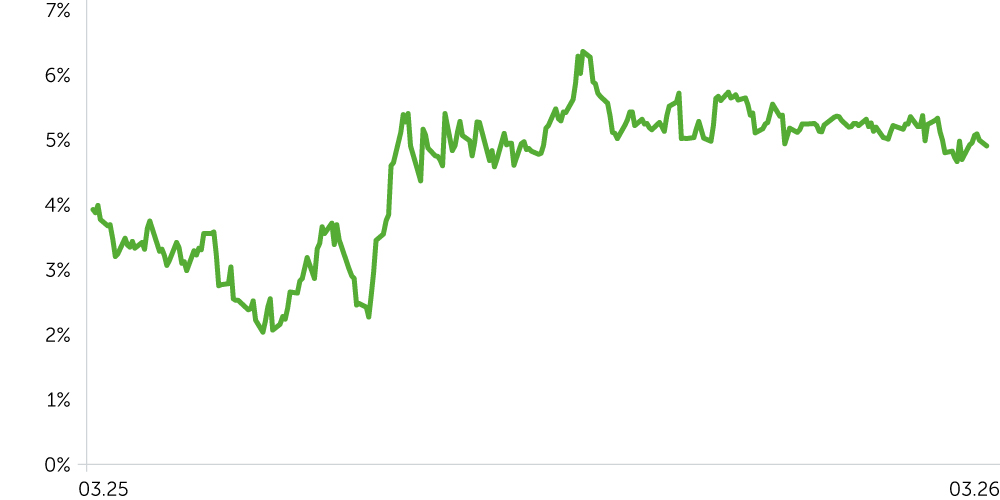

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

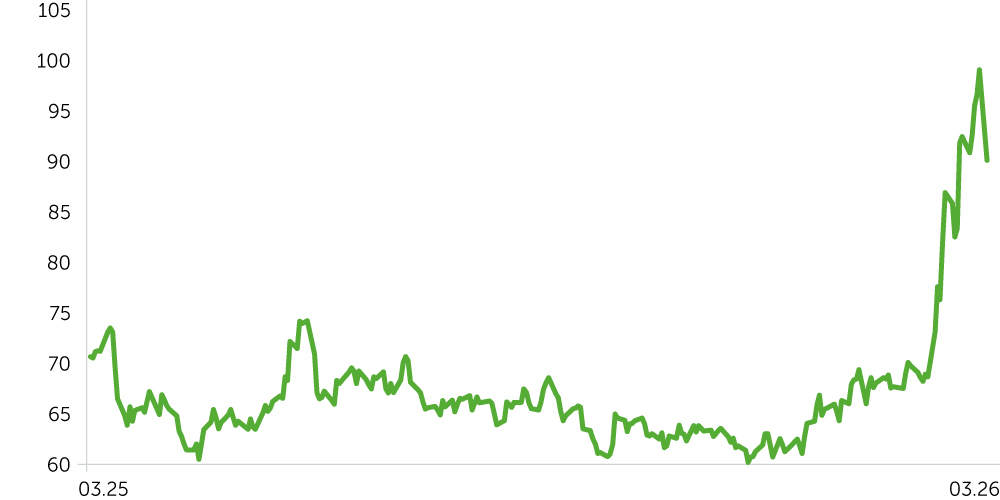

Brent Oil, 1-Year Dynamics

Between March 9 and March 23, 2026, UAE equity markets came under sustained pressure against the backdrop of the ongoing conflict involving the U.S., Israel, and Iran, as well as disruptions to shipping through the Strait of Hormuz. The Dubai Financial Market Index declined 6.4% (5,754 → 5,383), while the Abu Dhabi Securities Exchange Index fell 4.5% (9,863 → 9,423). For context, the S&P 500 corrected 3.2% over the same period (6,796 → 6,581), underscoring more pronounced downside in regional assets.

In contrast, Brent crude rose 6.1%, from $94 to $100 per barrel. Intraday price action was significantly more volatile. On March 9, Brent spiked to an intraday high of $119.50/bbl — the highest level since 2022 — before retracing and stabilizing near $100/bbl by period-end, as negotiations showed only limited progress.

Sector performance was broadly negative, with cyclical segments bearing the brunt of the sell-off. Real Estate was the clear underperformer, with an average two-week return of –13.44%. Aldar Properties fell 15.1%, Emaar Properties declined 14.3%, Emaar Development dropped 13.6%, and RAK Properties lost 21.0%. The move reflects a sharp slowdown in activity. In the first half of March, the total value of completed real estate transactions in the UAE declined 51% MoM and 31% YoY, pointing to a wait-and-see stance amid elevated uncertainty.

In contrast, Energy proved the most resilient segment, with an average return of –0.64% despite a challenging backdrop. Investors continue to position UAE energy names as direct beneficiaries of higher global hydrocarbon prices; even as logistical disruptions persist. The relative stability of ADNOC Gas (–0.3%) highlights confidence in the company’s operational resilience. Despite temporary adjustments linked to disruptions in the Strait of Hormuz, core assets — including the Habshan complex — remain fully operational, with deliveries continuing under transaction-by-transaction coordination.

Yields on UAE proxy government bonds moved higher, rising 8 bps from 4.81% to 4.89%. Over the same period, U.S. Treasuries saw a sharper repricing, with yields climbing 25 bps from 4.23% to 4.48%. As a result, the spread compressed from 58 bps to 42 bps. The move reflects two-sided pressure: on one hand, rising inflation expectations driven by the oil shock; on the other, a partial flight to quality into more liquid global assets.

Economic Updates

- Oil Shock and the Strait of Hormuz. Before the onset of hostilities, roughly 20mb/d of crude and refined products transited the Strait of Hormuz — about 19% of global consumption (105.14mb/d as of February 2026). Adjusting for the potential rerouting of ~5.5mb/d outside the strait, the net supply shock is estimated at 12–14mb/d, or 11–13% of global demand. Our base case assigns a 60% probability of reopening by mid-April, rising to 84% by mid-May and 94% by mid-June. This is notably more optimistic than market pricing: Polymarket implied just a 25% probability of normalization by April 30 as of March 18, down from 55% a week earlier.

- UAE Central Bank Stability Measures On March 17, 2026, the Central Bank of the United Arab Emirates introduced a Financial Institution Resilience Package aimed at preserving financial stability amid the regional conflict. Backed by >$272bn in FX reserves, the package is designed to ensure uninterrupted functioning of the banking system. Measures include expanded liquidity access, regulatory relief on liquidity requirements, release of capital buffers, greater flexibility in NPL classification, and targeted support for the domestic economy. Total liquidity available to banks is estimated at ~$250bn, providing a substantial buffer against potential financial stress.

Corporate News

- Major M&A: Multiply Group and 2PointZero On March 19, Multiply Group announced plans to merge with 2PointZero and Ghitha Holding, all within the International Holding Company ecosystem. The transaction will create a ~$32.6bn investment platform, targeting synergies through AI-driven strategies and expansion across 85+ countries. The market reaction was positive, with Multiply shares rising 10.8% over two weeks, leading gains in industrials. Management guides to ~35% net income growth in 2026, signaling an aggressive expansion trajectory despite elevated geopolitical risk.

- Amlak Finance (DFM: AMLAK). On March 8–9, Amlak Finance — the UAE’s largest Islamic mortgage provider — reported transformational FY2025 results, marking a turning point in the company’s history. Net profit surged ~117x, while total income jumped from ~$63m to $850m. The key driver was the $790m sale of a land bank in Ras Al Khor, generating $583m in profit. The transaction enabled the company to fully offset accumulated losses for the first time in 15 years and return to retained earnings. The stock rallied 26.4%, making it the top performer in the sector, reflecting both the scale of the earnings reset and balance sheet repair.

- Aldar Properties / Mubadala (ADX: ALDAR). Between March 10 and 13, Mubadala Investment Company, through its subsidiary Mamoura Diversified Global Holding, increased its stake in Aldar Properties from 25.12% to 26.26%. This follows a series of strategic initiatives, including a $2.72bn retail JV (Yas Mall, The Galleria Luxury Collection) and a $16.3bn expansion of the Al Maryah Island financial district. Despite strong fundamentals — +36% net profit, +47% revenue, and a record $19.5bn backlog in 2025 — Aldar shares declined 15.1%, reflecting geopolitical repricing rather than fundamentals.

- Air Aribia (ADX: AIRA). Air Arabia extended flight suspensions to several regional destinations, including Lebanon, Jordan, and Iraq, citing safety concerns. Operational capacity has fallen ~64% vs. pre-crisis levels, driving a 7.9% decline in the stock. At the same time, larger carriers such as Emirates and flydubai continue to operate a significant share of routes using secured air corridors and escort protocols. As of March 23, Emirates had restored ~75% of capacity, pointing to gradual operational normalization.

- ADNOC / Borouge (ADX: BORU). On March 19, ADNOC and OMV AG announced a key milestone in forming Borouge Group International AG, combining Borouge Plc, Borealis AG, and Nova Chemicals. An asset usage agreement for the Borouge 4 (B4) complex will enable commercialization of new capacity. The transaction is expected to deliver ~$400m in cumulative net income uplift over three years and support ~10% annual earnings growth post ramp-up. Upon completion (expected by end-March 2026), the combined entity will control 13.6mt of capacity across the Middle East, Europe, and North America, positioning it among the top four global polyolefin producers.

Two-Week Outlook

The trajectory of UAE markets will continue to be driven primarily by developments in the regional conflict. The Strait of Hormuz remains effectively closed to full-scale shipping. Prior to the conflict, roughly 20mb/d of crude and refined products transited the strait, accounting for ~19% of global consumption. The UAE, exporting around 3.2mb/d via Hormuz, retains the ability to reroute up to 1.5mb/d through the Habshan–Fujairah (ADCOP) pipeline, partially mitigating supply disruptions. Market attention is increasingly shifting to the credibility of de-escalation signals. Headlines around potential U.S.–Iran talks have already triggered a partial rebound in risk assets, with the Dubai Financial Market Index gaining 0.8% on the last trading day.

In our base case, we assign a 60–84% probability of normalization by mid-April to May, alongside a potential retracement in oil prices toward ~$60/bbl by May–June 2026. In a downside scenario, a prolonged blockade could trigger demand destruction dynamics, pushing oil prices above $200/bbl from June onward.

Against this backdrop, UAE equity markets are likely to remain highly volatile. Defensive segments — telecommunications, consumer staples, and parts of diversified financials — should continue to demonstrate relative resilience. By contrast, real estate, airlines, and logistics remain the most geopolitically sensitive sectors. At the same time, the strength of the UAE banking system — with capital adequacy ratios comfortably above regulatory thresholds — provides a solid buffer for financial stability, even under a prolonged stress scenario.