Investment Review №333. Right to hedge

This is not the time to take risks

By the middle of the second decade, the Emirates' stock markets were down slightly.

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

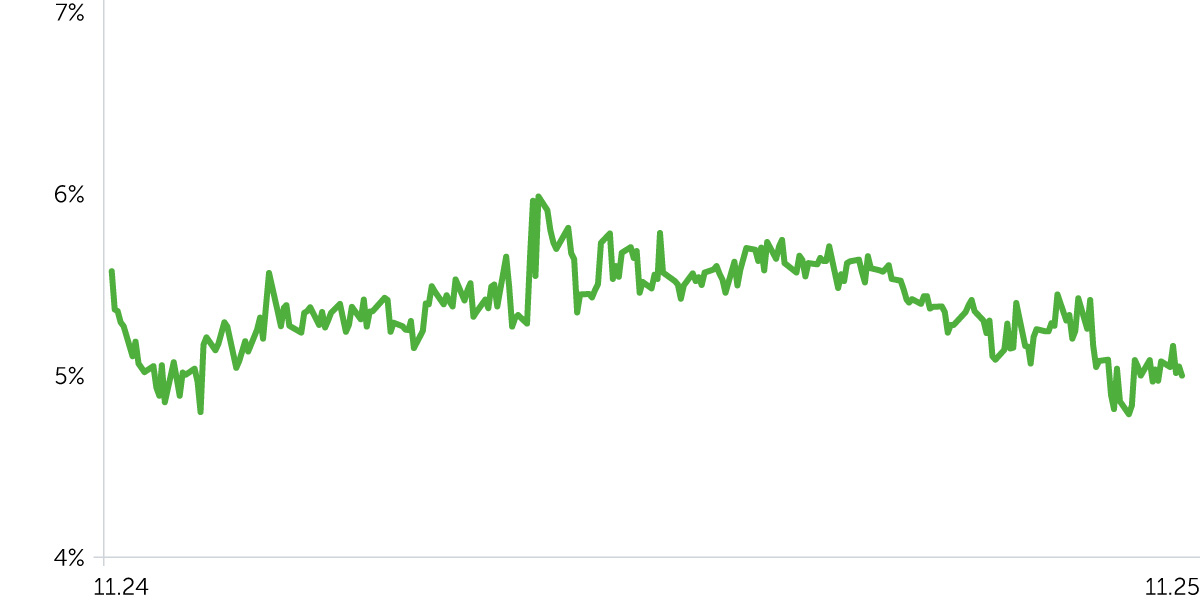

Yield, Forward Rate 1m10y, UAE, 1-Year Dynamics

Brent Oil, 1-Year Dynamics

Between November 3 and 17, 2025, UAE equity markets mirrored the global risk-off move. The Dubai Financial Market Index (DFM) declined by 1.0%, while the Abu Dhabi Securities Exchange (ADI) slipped 1.1%. For comparison, the S&P 500 shed 2.6% over the same stretch. The correction coincided with a more hawkish tone from the Federal Reserve and a sharp drop in market-implied odds of a December rate cut. This shift triggered a third consecutive week of losses across UAE exchanges, compounded by additional pressure from weakening oil prices.

Sector moves were largely negative. The best performer was Utilities (+2.75% over the two-week period), supported by solid results from TAQA and steady dividend flows. Consumer Discretionary also managed a modest gain (+0.40%). In contrast, several sectors underperformed the broader market: Financials (–1.6%), Energy (–2.09%), Industrials (–2.86%), Real Estate developers (–1.87%), Communication Services (–2.09%), and Consumer Staples (–3.24%). Within Financials, SHUAA Capital delivered a notable upside surprise, reporting net profit of AED 198 million for the first nine months of 2025—a sharp turnaround from a loss in the prior year. The result marked a key milestone in the company’s restructuring process.

The yield on 10-year UAE sovereign bonds held steady at approximately 5.13%, while the yield on 10-year U.S. Treasuries rose to 4.139%. As a result, the yield premium of UAE bonds over USTs narrowed to around 99 basis points, down from roughly 102 basis points two weeks earlier.

Economic Updates

- The non-oil private sector continues to underpin the UAE’s economic momentum. According to S&P Global, the country’s composite PMI held above 53 in October, while Dubai’s reading climbed to 54.5—the highest level since January. The data reflect solid expansion in new orders and output, accompanied by moderate cost pressures and more cautious hiring by firms.

- The real sector continues to affirm the resilience of domestic demand. According to Dubai authorities, the emirate’s GDP grew roughly 4–5% y/y in the first half of 2025, driven by trade, tourism, financial services, and construction. Abu Dhabi is recording double-digit increases in tourist arrivals and RevPAR, with hotels maintaining high occupancy rates, which strengthens the services sector’s contribution to UAE GDP and supports consumer spending. Additionally, rising FDI inflows into logistics and the digital economy further solidify the country’s position as a regional investment hub.

Corporate News

- Abu Dhabi National Energy Company (TAQA) reported revenue of AED 42.7 billion for the first nine months of 2025, marking a 2.9% year-over-year increase. Net profit reached AED 6.1 billion, while EBITDA totaled AED 16.0 billion. Capital expenditures surged 47% to AED 8.9 billion, reflecting accelerated investment in regulated networks and generation projects.

- SHUAA Capital recorded net profit of AED 198 million for the first nine months of 2025, compared with a net loss of AED 138 million in the corresponding period of the previous year. The improvement highlights progress in its capital optimization and cost-reduction initiatives, with the cost-to-income ratio improving to 92% from 103%.

- ADNOC Gas delivered strong Q3 2025 results, with earnings boosted by higher domestic volumes and an optimized contract portfolio. The company announced a shift to quarterly dividend payments, which enhances the dividend appeal of the broader ADNOC group.

Two-Week Outlook

Oil prices may trend sideways in the near term. Support is currently being provided by reduced hydrocarbon exports from Russia, following strikes on its oil and gas infrastructure and sanctions targeting Rosneft and Lukoil. A short-term price uptick could also be driven by a rise in geopolitical risk premiums. However, the fundamental outlook remains tilted to the downside. Notably, OPEC+ raised its production quotas by 137,000 barrels per day for both November and December, bringing the total increase since the start of the year to 2.88 million barrels per day. The completion of maintenance at Kazakhstan’s largest oil field, Tengiz, along with a surge in U.S. crude production to a record 13.86 million barrels per day, is expected to exert additional downward pressure on oil prices.

The risk outlook for UAE equities remains mixed. A reduced likelihood of a December rate cut by the Federal Reserve has heightened market volatility and kept yields elevated. At the same time, continued expansion in the UAE’s non-oil economy and strong corporate earnings are laying the groundwork for renewed interest in local dividend plays. Over the next two weeks, we expect the Dubai Financial Market (DFM) and Abu Dhabi Index (ADI) to exhibit a mildly downward bias. Utilities and high-quality banks appear best positioned to weather near-term headwinds, while developers and industrials are likely to remain more sensitive to interest rate dynamics and shifts in global risk appetite. From a technical perspective, the picture is still rather negative: the DFM index has slipped below its 50-day moving average and has yet to reach oversold territory on the RSI.