Investment Review №346. Riding the Green Wave

A delicate balance

Despite ongoing external uncertainty, the UAE’s stock indices posted moderate gains

DFM General Index: 1-Year Dynamics

Abu Dhabi Securities Exchange Index: 1-Year Dynamics

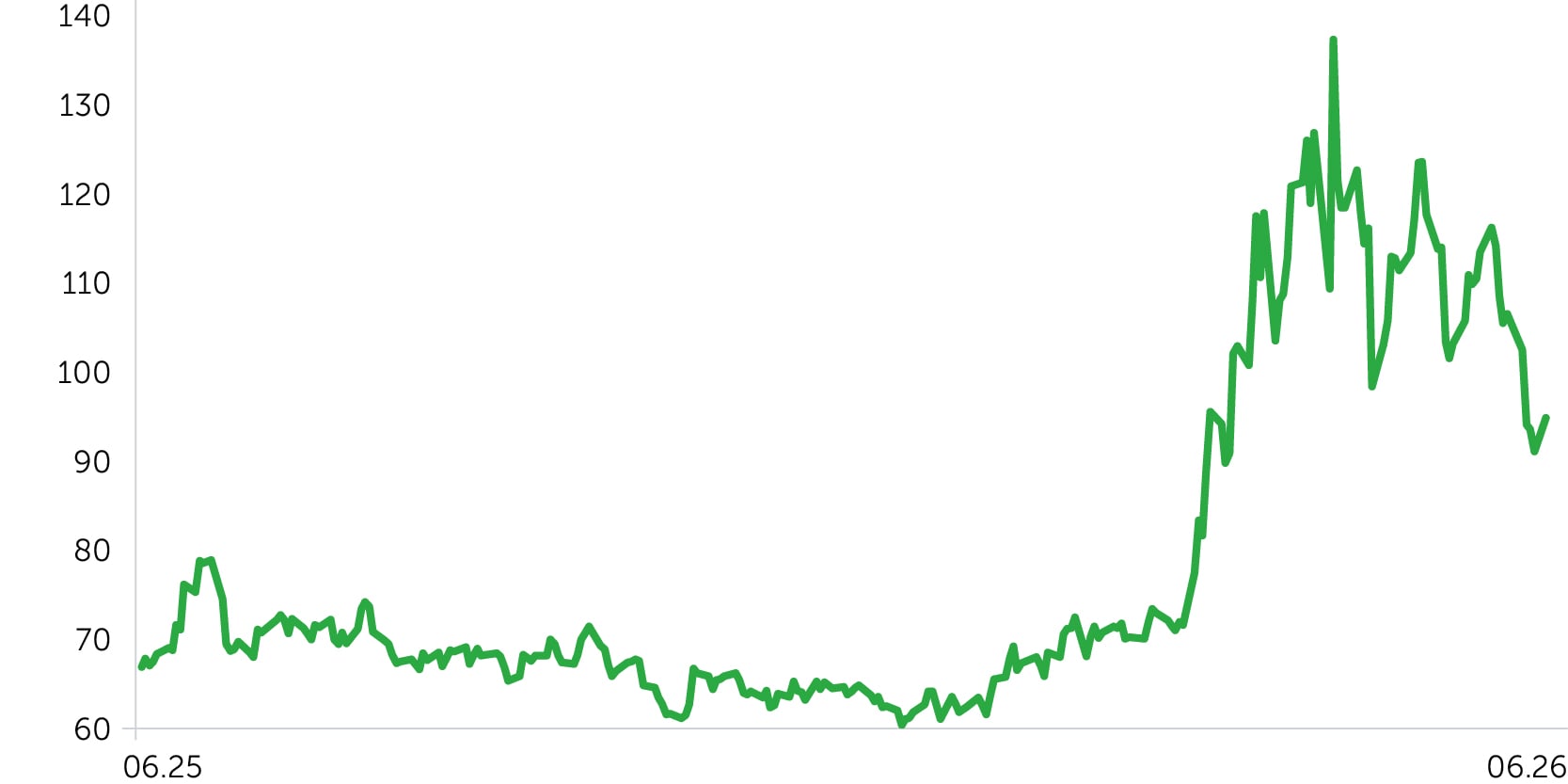

Brent Oil, 1-Year Dynamics

Over the two-week period from May 18 to June 1, 2026, UAE indices posted moderate gains, supported by a stabilizing geopolitical backdrop and solid Q1 2026 earnings. The Dubai Financial Market General Index (DFMGI) rose from 5,610 to 5,775 points (+2.9%), while the Abu Dhabi Securities Exchange General Index (ADXGI) added 0.9% to 9,651 points from 9,561. By comparison, the U.S. S&P 500 Index gained 2.7% over the same period, whereas Brent crude fell 18.6% to $95 per barrel from $117 on de-escalation hopes around the Strait of Hormuz.

Sector performance in the UAE market was predominantly positive. Top performers were Consumer Discretionary (+9.63%), Industrials (+8.69%), and Consumer Staples (+6.37%), indicating demand is broadening beyond defensives. Within Consumer Discretionary, Americana Restaurants International (+13.07%) and Parkin Co. (+7.56%) were key contributors. In Industrials, Multiply Group (+13.54%), Aramex (+6.32%), and Dubai Investments (+5.71%) led growth. Strength across the industrial/logistics complex reflects ongoing demand for infrastructure and transportation themes and the resilience of logistics and services providers. Real Estate and Utilities also closed higher (+3.30% and +3.25%, respectively). Communication Services was the sole laggard over the review period (-0.93%). The pullback in e& was largely technical and industry-specific: after a strong post-earnings rally, some investors took profits, and a moderate risk-off tone with rotation into cyclicals left telecoms as the only sector in negative territory despite a constructive fundamental backdrop for this group.

The UAE 10-year sovereign proxy yield ended the period at 5.03%, up from 4.99% (+3.7 bps), while the 10-year U.S. Treasury yield declined from 4.74% to 4.53% (-21 bps). The UAE–U.S. 10-year yield spread widened from ~25 bps to ~50 bps, driven by slightly higher local bond yields alongside lower rates on U.S. Treasuries.

Economic Updates

- In late May 2026, the Emirates News Agency (WAM) released final 2025 GDP data: UAE real GDP grew 6.2% YoY to $517.3bn, while non-oil GDP expanded 6.8% to $408.4bn. Growth was driven by construction, financial services, insurance, real estate, and transportation.

- The S&P Global UAE PMI rose to 52.6 in May 2026 from 52.1 in April, indicating a modest improvement in non-oil business conditions. Meanwhile, in April, the PMI had eased to 52.1 amid pressure from the Iran-related conflict on tourism and shipping.

- According to the Dubai Statistics Center, Dubai inflation accelerated to 4.8% YoY in April 2026 from 3.8% in March. In the base case, inflation is projected to peak at 5.4% in May and ease to 2.9% in December 2026.

- On 1 May 2026, the UAE formally exited OPEC and OPEC+. The move paves the way for higher output without quota constraints, potentially to 5.0 million barrel per day (mb/d), up from roughly 3.4 mb/d prior to the conflict.

Corporate News

- International Holding Company reported Q1 2026 results: revenue was $8.5bn and earnings after tax reached $2.2bn (+98.5% YoY). Management plans to invest up to $8bn in mining, energy, and financial services over the next six months.

- e& posted Q1 2026 revenue of $5.3bn (+15.1% YoY) and net income of $0.8bn, supported by subscriber growth to 248 million (+30.8% YoY). Over the two-week review period, the Communication Services sector declined 0.93%, and e& stock dropped about 1.7%, while du closed slightly higher.

- First Abu Dhabi Bank reported Q1 2026 net income of $1.4bn and operating income of $2.5bn (+6% YoY), delivering a 17.8% return on equity.

- Aldar’s Q1 2026 net income rose 20% to $0.6bn, with revenue up 12% to $2.4bn. The value of pending projects in the pipeline totaled $16.9bn.

- Aramex reported Q1 2026 revenue of $0.4bn (+2% YoY), with domestic express up 11%, freight forwarding rising 7%, and logistics up 9%.

- Indian regulators granted final approval for Emirates NBD to acquire a controlling stake in RBL Bank via an investment of approximately $3.0bn.

Two-Week Outlook

Uncertainty in the oil market remains elevated, with developments around the Strait of Hormuz continuing to be the primary price driver. If the current “double-blockade” conditions persist, oil prices are likely to gradually move higher; by contrast, de-escalation and a reopening of the Strait would likely trigger a sharp pullback. In the near term, three factors should drive the UAE market: the oil price trajectory and the Strait of Hormuz scenario, the resilience of Q2 2026 earnings, and the pace at which the geopolitical risk premium normalizes in local assets.

Base case: robust earnings from ADNOC Group, utilities, banks, and logistics companies should sustain interest in UAE large caps. Cautious case: rising global rates or an unexpected Middle East de-escalation would prompt rotation into defensives and further index consolidation.