Financier №4 (40) 2025

Tural Aliyev

junior analyst at Freedom Finance Global

Band Prices

How the Cost of Radio Frequencies Affects the Telecom Market

The revaluation of radio frequencies has become one of the most remarkable episodes in the history of telecoms. Over the past 30 years, mobile communications have transformed from a service for a select few into one accessible to virtually everyone. At the same time, bands have always been—and remain—a scarce resource, for which companies are willing to pay tens of billions of dollars.

It’s All About Technology

To launch a cellular network, an operator needs not only a tower, an antenna, and a switch, but also dedicated bands. The number of frequencies suitable for mass mobile communications is limited. Telecom companies compete for bands that provide wide coverage and an acceptable data transfer rate. Meanwhile, each successive generation of communications requires new spectrum allocations. 2G operated within certain bands, 3G and 4G in others, while additional spectrum was allocated for the development of 5G.

The mobile communications boom of the 2000s turned radio frequencies into one of the most valuable intangible assets on companies’ balance sheets. Auctions used to allocate them became a source of excess revenue for government budgets and, at the same time, a cause of debt crises for operators.

Demand for Spectrum

The first series of auctions for 3G network deployment in 2000 demonstrated how highly the market was willing to value the “air.” The UK government earned £22.5 billion from the sale of frequencies, while Germany earned €50.8 billion. Businesses expected to quickly recoup the costs of purchasing the spectrum through increased revenues from the services provided.

However, reality turned out differently. German operators E-Plus and VIAG Interkom went bankrupt just one year after winning the auctions. Their revenues failed to rise to levels that would have allowed them to easily service their loans. The experience of these operators showed that purchasing radio frequencies can be not only a source of growth, but also a cause of crisis.

In high-income countries, up to 84% of the population is connected to 5G networks, while this share is only 4% in poorer regions

Two decades later, a similar story unfolded in the United States. In 2021, the world’s largest 5G spectrum auction took place there, with total bids exceeding $81 billion. The bulk of the spectrum went to the leading American telecom companies—Verizon (VZ) and AT&T (T). By deploying new networks, these companies expected to quickly recoup the funds spent on purchasing radio frequencies. However, these expectations were also not met: operators’ profits declined due to rising debt levels. The companies were forced to revise their investment programs, which led to a drop in share prices.

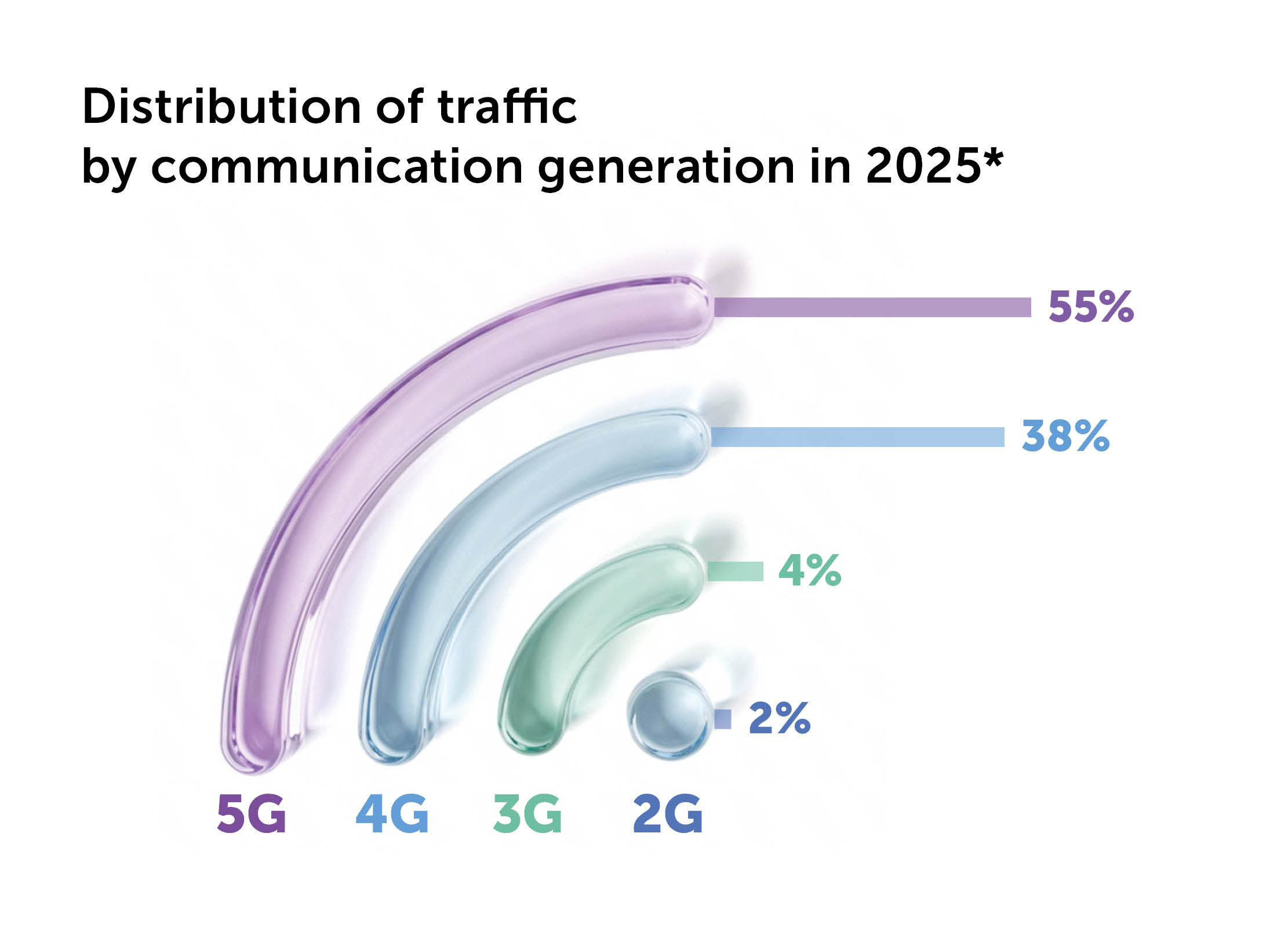

*1% is accounted for by other communication technologies. Source: itu.int

Cooling-Off Period

By 2024–2025, telecom companies had gradually shifted to a more pragmatic approach to radio frequencies. Operators became more cautious in assessing expected investment returns and the impact of debt on their businesses.

For example, at an auction held in Poland in 2025, the final sale price for frequencies used for rural and suburban coverage exceeded the starting price by only 3.6%, whereas ten years earlier, prices could have risen by tens of percent during the bidding process. This balanced cost approach allowed local industry participants to maintain financial stability and preserve resources for further investment.

The example of India is even more telling. There, spectrum worth nearly 962 billion rupees (approximately $11 billion) was auctioned in 2025, but only 113 billion rupees (around $1.25 billion) was ultimately sold. Local operators deliberately chose not to acquire most of the spectrum to avoid accumulating debt for benefits that remain uncertain in the distant future.

Incidentally, according to the Global Satellite Suppliers Association (GSA), the average price of 5G spectrum in 2024 was eight times lower than its peak in 2021. Spectrum bands have ceased to be objects of speculation.

Time for Rationality

In the early 2000s, government budgets earned colossal one-time revenues from spectrum auctions. A few years later, however, governments in many countries began to see the other side of the coin. Debt-laden operators were cutting investment, postponing network upgrades, and raising subscriber tariffs. As a result, the rules of the game in this market changed significantly.

Governments now exercise greater control over radio frequency pricing. To this end, requirements for infrastructure development and increased accessibility of mobile communications have been included in auction terms. Poland, mentioned above, now requires operators receiving new spectrum bands to ensure 90% nationwide 5G coverage by 2027. France and the Czech Republic, meanwhile, use subsidy and co-financing mechanisms to partially compensate operators for the costs of building networks in less profitable regions. At upcoming spectrum auctions in the United States, part of the proceeds will be allocated to network modernization and the replacement of Chinese-made equipment under the national Rip and Replace program. This approach reflects a new model: the focus shifts from maximizing auction prices to maximizing the impact on users and national infrastructure.

In Switzerland, where mobile internet is considered the most expensive in the world, the average cost of 1 GB of mobile data is $7.29

How Much Does a Gigabyte Cost?

Any decision on spectrum pricing ultimately affects subscriber tariffs. Where competition is intense, operators try not to fully pass on their costs to consumers. Companies optimize networks, share infrastructure, and implement joint tower construction projects. In markets with fewer participants, costs are usually passed on to subscribers, though this typically occurs through gradual price increases.

Even when tariffs rise moderately, every user feels the impact of expensive auctions. High license fees slow the adoption of new technologies: operators delay the launch of 5G or the expansion of coverage, maintain older standards for longer periods, and upgrade equipment less frequently.

Lower spectrum costs have the opposite effect. In Europe, communications tariffs increased by less than 2% in 2024, while operator investment in infrastructure rose by nearly 10%. Regulators are tightening oversight of telecom pricing policies, while the industry benefits from tax incentives, easier access to financing, and shared infrastructure initiatives.

As a result, regulatory quality and market structure are becoming as important for investors in valuing telecom companies as margins or market share.

Photo: open sources

New Cycle: 6G

The industry is approaching a new milestone—the transition to the 6G standard. According to industry estimates based on the International Telecommunication Union (ITU) IMT-2030 roadmap and forecasts from equipment manufacturers, the first commercial 6G solutions will appear around 2030. Tests of the new communication format already demonstrate data transfer speeds of approximately 100 Gbps over distances of about 100 meters. For comparison, the maximum performance of 5G is estimated at roughly 5 Gbps.

The deployment of 6G networks will require the allocation of new radio frequencies in the 7–15 GHz range, triggering another cycle of spectrum redistribution. However, the rules of the game are likely to differ from those of the “expensive bands” era. Instead of record-breaking prices, companies will commit to accelerated infrastructure deployment. Winners of future auctions will gain the ability to manage spectrum portfolios like other assets—optimizing allocation, timing, profitability, and debt burden.