Financier №4 (40) 2025

Vadim Merkulov

director of the analytical department at Freedom Finance Global

Attention economy

New growth points for the telecom industry

The boundaries between telecommunications, internet services, and media are increasingly blurred. Telecommunications companies provide channels for the distribution of goods, services, and content, while digital platforms control distribution, advertising, promotion, and audience engagement.

Structural Transformation

In September 2018, analysts at Standard & Poor’s and MSCI revised the Global Industry Classification Standard (GICS), which is widely used by the world’s largest investors. A new sector- Communication Services - was introduced, combining traditional telecom operators with leading social media platforms (Meta, META), internet corporations (Alphabet, GOOGL), and streaming companies (Netflix, NFLX). In 2023, the sector’s market capitalization grew by 55.8%, followed by a further 40% increase in 2024. Growth reached nearly 20% year on year in the first ten months of 2025.

The sector is subdivided into two major segments: Telecommunication Services and Media & Entertainment. Alphabet (16.5%), Meta (14.8%), and Netflix (5.9%) currently lead the sector by share of total market capitalization.

Service Fees

The sector’s expansion is being driven by increased efficiency in digital advertising and changes in content consumption patterns, which have significantly improved financial performance across the internet industry.

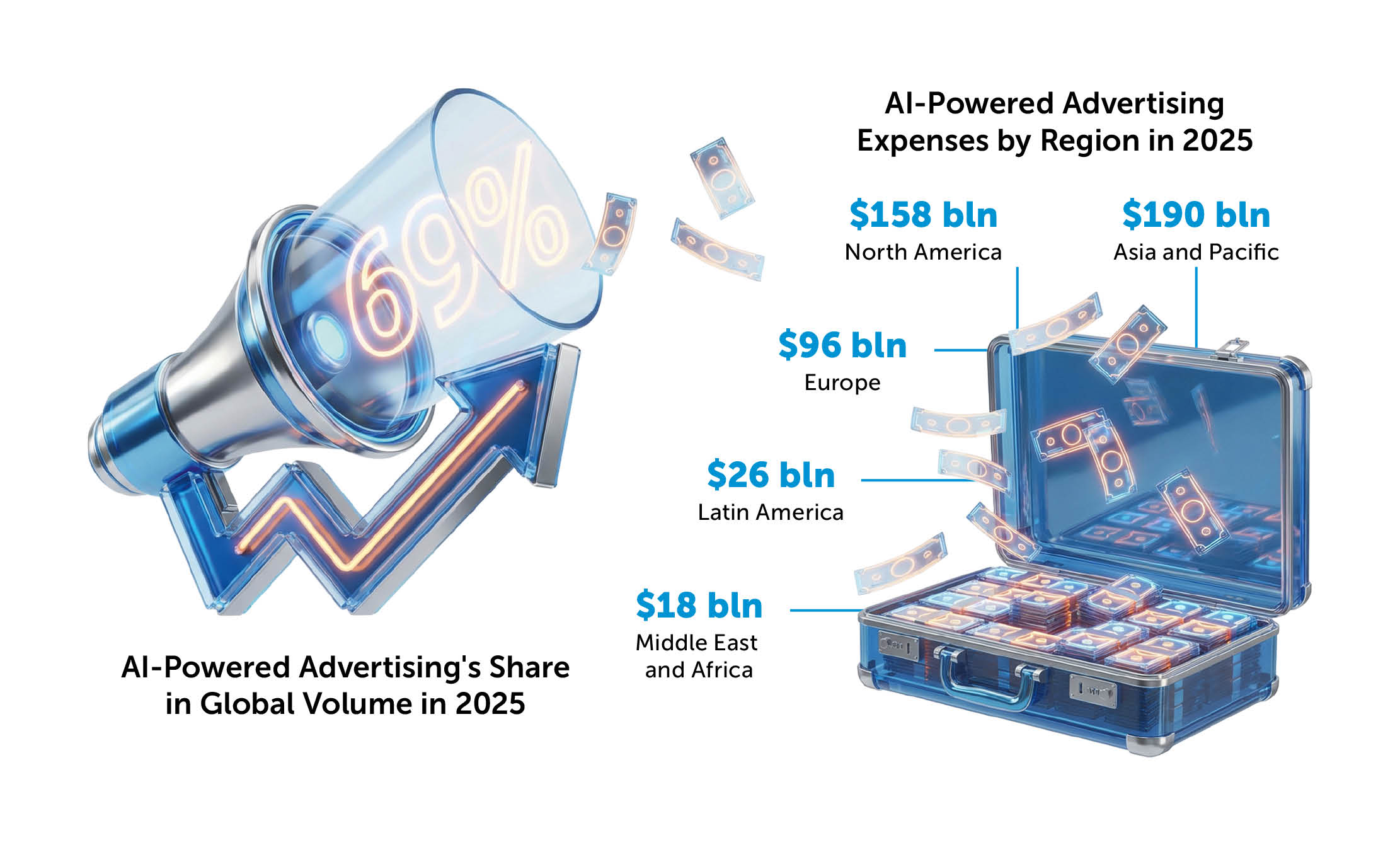

The widespread adoption of AI tools in advertising has enabled leading digital platforms to increase their return on advertising spend (ROAS) - a metric measuring the ratio of advertising revenue to advertising costs - while requiring fewer manual adjustments. This efficiency has encouraged advertisers to redirect budgets towards these platforms, resulting in sharp revenue growth among internet giants. In the third quarter of 2025, Alphabet’s revenue rose by almost 16% year on year to $102.3 billion, while Meta’s revenue increased by 26% to $51.24 billion, with 98% generated from advertising.

At the same time, viewing habits continue to evolve. In May 2025, according to Nielsen marketing research, streaming’s share of total TV consumption in the United States surpassed the combined share of broadcast and cable television for the first time. Analysts believe this marks a fundamental shift in media consumption. Nielsen forecasts that total digital advertising expenditure in the US will reach $33.35 billion by the end of 2025, representing 15.8% year-on-year growth, and that traditional television advertising will be overtaken by digital platforms by 2028. Subscriber bases at Netflix and Amazon Prime Video have expanded severalfold over the past two years, supported in part by exclusive sports broadcasting agreements. For example, Amazon Prime will broadcast NBA games during the 2025/26 season.

At the Last Frontier

Within the Communication Services sector, telecommunications companies retain their own growth opportunities. According to McKinsey, industry profits could increase by up to 35% through the adoption of digital technologies. Replacing call-centre operators with AI solutions reduces customer support costs, while optimizing cell tower placement through subscriber mobility analysis lowers infrastructure deployment and maintenance expenses.

A key growth driver is the so-called last mile - the final segment of the network connecting an operator’s node to the end user’s home or office. This segment largely determines connection speed and quality. The United States is currently undergoing a large-scale modernization of last-mile infrastructure, enabling providers to significantly increase household internet speeds and transition customers to higher-priced service plans.

In urban areas, operators are deploying Fibre to the Home (FTTH) solutions, while in rural and suburban regions they rely on Fixed Wireless Access (FWA), a 5G-based technology that delivers ultra-high-speed broadband without the need for additional cabling. By June 2025, AT&T (T) had provided fibre-optic connections to 30 million households, T-Mobile (TMUS) to 9.5 million, and Verizon (VZ) to 7.7 million. By 2030, all three operators plan to double these figures.

The Industry Laid Bare: An Investor’s Insight

The situation in the Communication Services sector offers a rare combination of factors to stock market participants.

Firstly, its growth is driven by long-term market and technological trends: advertising is moving to the Internet and streaming TV, demand for fast home Internet is steadily increasing, and AI helps to earn more from advertising and optimizes the work of operators.

Secondly, as noted in the McKinsey report, telecommunications companies have already passed the peak of 5G construction costs. Now they have more funds available, which they can either return to shareholders through dividends or share redemption, or spend on strategic M&A (mergers and acquisitions) transactions. This will help industry representatives embody a solid growth potential.

Thirdly, companies in the industry provide their shareholders with a modest but stable dividend. The Communication Services SPDR ETF (XLC), made up of industry securities, makes quarterly payments with a yield of about 1% per annum, as the priority for the sector is to increase capital and investment in development, rather than distributing a large portion of profits to shareholders. At the same time, the growth of the Communication Services SPDR ETF itself exceeded 20% from January to September 2025. This secured the fund a place in the Top-3 in terms of profitability in the US market. For an investor, the only drawback of an industry–specific ETF is its high proportion of online platforms that depend on advertising. In the event of a slowdown in business activity, this market will shrink significantly, followed by a fall in the profitability of the fund. An alternative to XLC can be stock indexes for the communications sector (RSPC), which reduce dependence on two or three names and add importance to the “middle” represented by regional and gaming companies, as well as media holdings. The dividend yield of their shares hovers around 1.5%.

Focus on Acceleration

McKinsey's baseline scenario for the 12-24 month horizon assumes growth in the Communication Services sector. In the digital advertising segment, figures are expected to grow at double-digit rates driven by AI; streaming will continue to expand; more households will use fiber-optic last-mile communications. McKinsey also forecasts moderate profit growth in the sector.

The active development of the telecom industry's services segment is driven by the creation of a new “attention economy” infrastructure. This infrastructure is built on the rapid penetration of broadband internet, reaching a huge audience, and distributing goods and services. People need high-speed internet, and advertisers are interested in access to potential customers. Fulfilling these needs will contribute to the continued growth of the industry's market capitalization.