Financier №4 (40) 2025

Sergey Glinyanov

senior analyst Freedom Finance Global

Space as a Signal

What Competition Between Satellite and Mobile Internet Could Lead To

Near-Earth space has become a new competitive arena for major telecommunications companies seeking leadership in satellite internet and communications. Market participants are racing to secure positions in this rapidly expanding segment, which, according to ABI Research, is expected to reach nearly $240 billion by 2030.

Cheaper at Scale

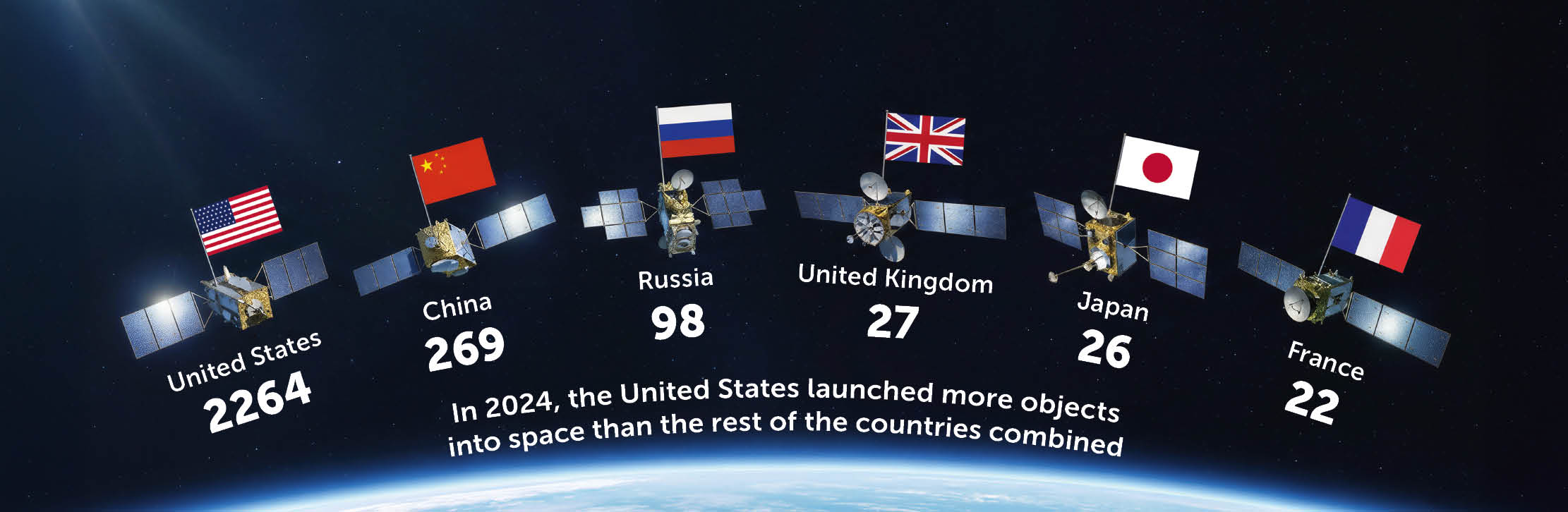

Until the mid-2010s, satellite communications were largely regarded as a costly niche technology with limited practical use. This perception began to change in 2015, when SpaceX introduced reusable Falcon rockets, dramatically reducing the cost of launching payloads into orbit.

According to data from the US Center for Strategic and International Studies (CSIS), two decades ago launching one kilogram of cargo into orbit cost nearly $50,000. Today, the figure has fallen to around $1,500, and is expected to decline further once SpaceX’s Starship enters mass operation. These cost reductions have made possible a new format of connectivity based on low Earth orbit (LEO) satellites.

According to ABI Research, the number of operational satellites increased from 3,200 in 2020 to 11,500 in 2024, largely due to the deployment of orbital relay constellations. This number is expected to grow severalfold in the coming years.

Satellite internet providers are increasingly competing with mobile operators. Today, satellite-based internet services offer latency of around 20 milliseconds and data transmission speeds of 100–200 Mbps—comparable to early-stage 5G performance.

According to Omdia, the primary users of satellite internet services include:

- residents of remote areas without access to wired broadband or mobile networks;

- transport and logistics companies, for which connectivity provides both competitive advantage and additional revenue opportunities;

- corporate and government customers operating in isolated locations, such as geological survey teams, meteorological and polar stations, military bases, and emergency services;

- travelers who require reliable connectivity regardless of location.

Satellite internet has become a breakthrough technology for developing regions where terrestrial infrastructure is absent or underdeveloped. Omdia forecasts that the number of satellite internet users in Africa will grow by 140% between 2022 and 2030, improving access to education, enabling telemedicine, and supporting broader economic development.

By 2030, the number of LEO satellites in orbit is expected to exceed 72,000, according to analysts at J’son & Partners.

Space Race Frontrunners

- SpaceX’s Starlink remains the clear leader in the satellite communications market and has become a major revenue generator within Elon Musk’s business portfolio. As of September 2025, Starlink’s constellation of approximately 8,000 satellites served more than 7.1 million subscribers worldwide. The company plans to expand the network to 42,000 satellites. Starlink’s financial performance has been equally impressive. Revenue rose from $1.4 billion in 2022 to nearly $8 billion in 2024, accounting for more than half of SpaceX’s total revenue. Recurring subscription payments represent roughly 80% of Starlink’s income, making its business model highly predictable. Analysts at Quilty Space estimate that Starlink’s revenue could reach around $12 billion in 2025. The company’s position was further strengthened by its acquisition of spectrum in the AWS-4 and H-block bands in the near-2 GHz range from EchoStar (SATS). This transaction significantly expands Starlink’s potential coverage for both satellite and mobile communications.

- OneWeb, the second-largest satellite communications provider and a subsidiary of Eutelsat (EUTLF), operates a constellation of approximately 650 satellites. It offers particularly dense coverage in polar regions, although coverage diminishes closer to the equator. As of August 2025, OneWeb’s ground infrastructure comprised 29 points of presence and 40 satellite network nodes worldwide.

- Amazon’s (AMZN) Project Kuiper ranks third in the sector. By September 2025, the company had launched more than 100 satellites and plans to expand its constellation to 3,200 units deployed across three orbital altitudes—590, 610, and 630 kilometers Under licenses issued by the US Federal Communications Commission, Amazon is required to place half of these satellites into operation by July 30, 2026, positioning the company to challenge for second place in the market.

Source: unoosa.org

Integrated Development

According to a report by Aerodoc, the future of telecommunications lies in the integration of satellite and terrestrial networks. A major breakthrough is expected from the combination of device-to-device (D2D) technology with satellite communications—a concept successfully tested in late 2024 by the European Space Agency (ESA) and Telesat (TSAT). Collaboration between mobile operators and satellite providers is accelerating. In March 2025, India’s Airtel (AARTY) signed an agreement with SpaceX to offer Starlink services, allowing the companies to expand mobile connectivity without extensive terrestrial infrastructure deployment. Similarly, T-Mobile (TMUS) has partnered with Starlink to provide Direct-to-Cell satellite services, eliminating mobile coverage gaps without the need to build additional towers.

Challenges and Constraints

Despite its rapid growth, the LEO satellite internet market faces significant challenges.

The most pressing issues include orbital congestion and the increasing volume of space debris. According to Starlink’s 2025 projections, between one and four of its satellites deorbit daily as they reach the end of their operational lifespan. The company states that these satellites undergo controlled atmospheric re-entry and burn up completely. Nevertheless, scientists and policymakers worldwide are calling for stricter regulation of near-Earth space.

Other constraints include limited radio spectrum availability and the complexity of coordinating global satellite traffic. Deloitte analysts note that further deployment of satellite services will be accompanied by tighter regulatory oversight. Spectrum allocation for satellite communications is increasingly regulated in the same manner as terrestrial telecom licenses, reflecting the scarcity of this resource even in orbit.

Some traditional telecom operators are pushing for regulatory harmonization, arguing that satellite providers should also be required to pay license fees, contribute to universal service funds, and comply with content regulations.

Even so, Deloitte concludes that competition between LEO satellite networks and terrestrial LTE and 5G operators does not signal the decline of traditional telecommunications. Instead, it represents the next stage in the sector’s evolution. Satellite connectivity creates opportunities for synergy, particularly for users in remote or underserved regions, where space-based networks remain the only viable gateway to the digital economy, online education, and healthcare.

Over the next five years, the contours of a hybrid telecommunications ecosystem—combining terrestrial and orbital networks—will take shape. Near-Earth space is poised to elevate global communications technologies to an entirely new level.