Investment Review №343. The return of the bulls

Corporate News in Focus of Our Analysts

TSMC Results

On April 16, TSMC (TSM-US) delivered one of the strongest prints in its history: revenue, margins, and EPS all exceeded expectations, driven by robust AI-driven demand for advanced nodes, effective cost optimization, higher capacity utilization, and a more favorable USD/NTD. The outlook is even more compelling than the report. The company’s Q2 FY26 revenue and margin guidance came in well ahead of consensus and our estimates. Management raised its full-year 2026 revenue growth outlook to over 30% in U.S. dollar terms (from ~30% in January) and now expects 2026 capex at the high end of the $52–56bn range. The AI accelerator revenue CAGR forecast was tightened to 57–59% (from 54–59%), and long-term profitability targets were reaffirmed. Smartphones were a bright spot: CEO Wei noted continued outperformance in premium handsets, a constructive signal ahead of Apple’s (AAPL) results. Management also highlighted the growing importance of CPUs in AI servers and an increasing CPU/GPU ratio, a trend that should benefit AMD (AMD) and Intel (INTC).

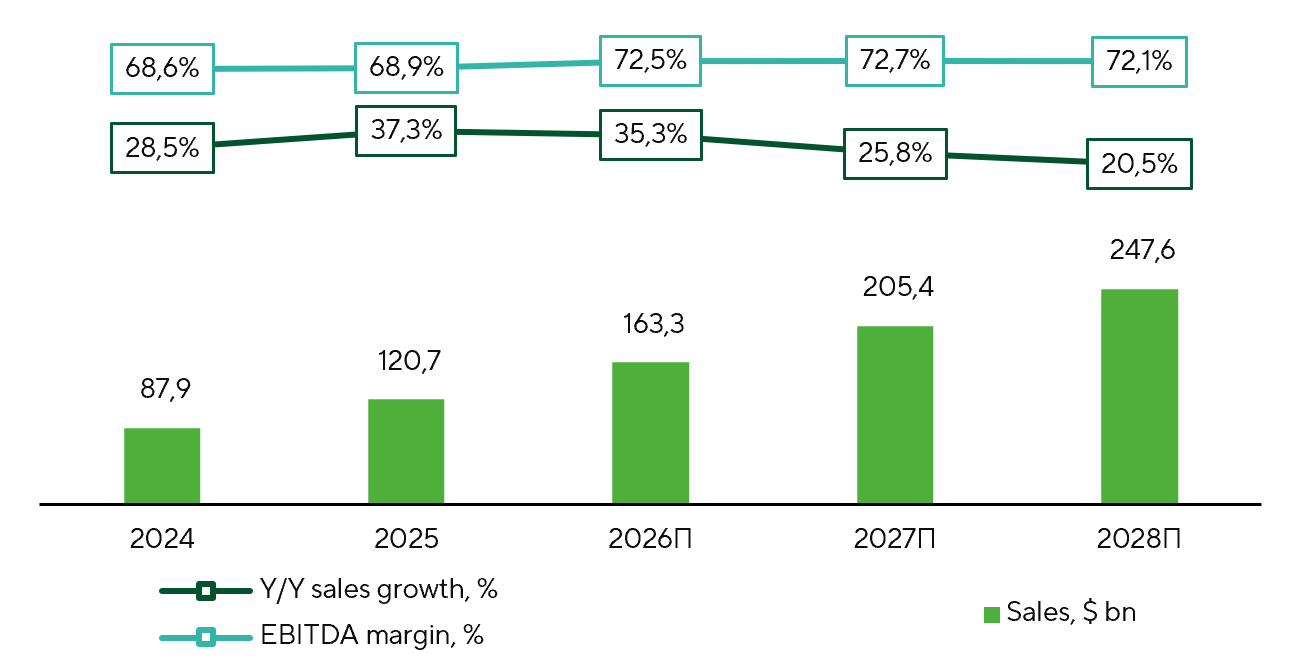

Key Financials of TSMC

Sources: TSMС, FactSet, Freedom Broker

Alcoa Results

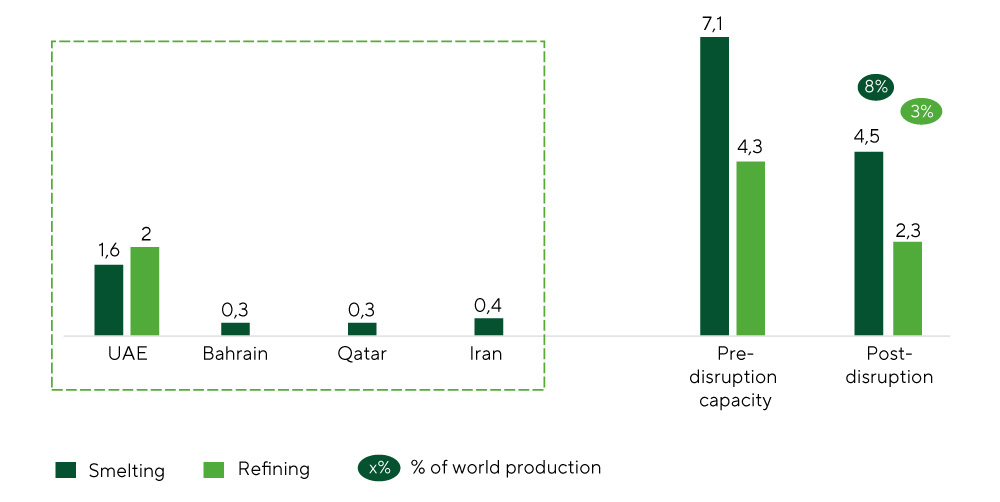

Alcoa’s 1Q26 results came in below both consensus and Freedom Broker revenue expectations, but earnings quality was stronger than the topline would suggest. Aluminum prices remained firm, and the shortfall in shipments appears transitory rather than structural. Guidance remains unchanged, and despite a softer revenue, the company is well positioned to benefit from the ongoing aluminum price rally. A key takeaway from the quarter is management’s confidence in a strong 2026. Management reiterated a constructive full-year profitability outlook, supported by resilient pricing, structural demand drivers, and a healthier balance sheet following the monetization of the Ma’aden JV. The commodity context remains the principal support for the stock. Aluminum prices have rallied amid heightened tensions involving Iran, which elevate the risk of supply disruptions in the Gulf region, responsible for roughly 9% of global aluminum production. As highlighted in our March Commodity Markets Report, rising Middle East tensions introduce additional upside risks to the aluminum market.

War in Iran impact on Aluminum markets

Sources: Freedom Broker, CRU, Alcoa

Bank Results

The largest U.S. banks posted generally solid 1Q26 results, though the composition of surprises varied by institution. JPMorgan Chase (JPM), Bank of America (BAC), Citigroup (C), Goldman Sachs (GS), and Morgan Stanley (MS) exceeded both revenue and earnings estimates, while Wells Fargo (WFC) saw softer interest income. In the lack of a broad-based beat-and-raise, banks reaffirmed resilient core operations and stable asset quality, with management commentary on momentum into 2026 serving as a key market driver.

For universal banks, net interest income (NII) and net interest margin (NIM) remain in focus. BAC was the only bank to raise its NII outlook; JPM trimmed guidance amid NIM pressure, while WFC and C kept forecasts unchanged. Across management teams, the message was that NII trajectories hinge on the balance of loan growth, funding costs, and the shape of the yield curve—implying no single sector-wide path.

Capital markets results remain solid, with banks citing robust client trading activity and a healthy investment banking pipeline. GS and MS are showing particularly strong momentum, while universal banks also highlight resilient M&A and ECM activity, underpinning expectations for fee income growth in 2026.

On costs, approaches diverge: JPM, GS, and MS are guiding to faster expense growth, while BAC, C, and WFC are prioritizing efficiency improvements.

Capital positions remain strong. GS, MS, BAC, C, and WFC expect neutral to positive Basel III impacts, while JPM, contrarily, is anticipating higher capital requirements. Overall, this should support continued capital returns to shareholders, albeit at varying paces across banks.

| Ticker | Efficiency | ∆ | EPS | ∆ | Book per share | ∆ | RoTE | ∆ | P/E | P / Tangible Book | Target Price | Current Price | Potential | ||||||

| LTM | NTM | p.p. | LTM | NTM | % | LTM | NTM | % | LTM | NTM | p.p. | LTM | NTM | LTM | NTM | ||||

| JPM | 52,9% | 53,8% | 0,9 | 20,9 | 22,1 | 6,1% | 125,0 | 138,2 | 10,6% | 20,4% | 19,9% | -0,5 | 14,9 | 14,0 | 2,88 | 2,67 | 335 | 310,3 | 8% |

| BAC | 62,3% | 60,2% | -2,1 | 4,0 | 4,5 | 12,4% | 38,0 | 41,0 | 7,9% | 14,6% | 15,7% | 1,1 | 13,4 | 11,9 | 1,86 | 1,76 | 65 | 53,9 | 21% |

| C | 63,5% | 59,3% | -4,2 | 8,1 | 11,0 | 36,8% | 108,4 | 122,0 | 12,5% | 8,3% | 10,9% | 2,6 | 16,4 | 12,0 | 1,34 | 1,23 | 147 | 132,2 | 11% |

| WFC | 65,0% | 62,9% | -2,1 | 6,5 | 7,2 | 10,5% | 52,3 | 57,5 | 10,1% | 14,8% | 15,2% | 0,3 | 12,6 | 11,4 | 1,81 | 1,69 | 103 | 81,4 | 27% |

| GS | 64,3% | 62,6% | -1,7 | 54,7 | 59,4 | 8,6% | 364,0 | 382,4 | 5,0% | 16,5% | 17,3% | 0,8 | 16,9 | 15,6 | 2,66 | 2,60 | 1000 | 926,0 | 8% |

| MS | 67,7% | 67,2% | -0,5 | 11,0 | 12,0 | 8,4% | 63,0 | 71,6 | 13,8% | 22,4% | 21,9% | -0,5 | 17,1 | 15,8 | 3,78 | 3,33 | 200 | 188,8 | 6% |

Comparison of U.S. Major Banks

Sources: FactSet, bank data, Freedom Broker analysis

JNJ 1Q26 Results

Another strong quarter for JNJ, with results ahead of Street expectations. Key growth drivers remain intact, with both business segments performing well. The significant decline in STELARA was fully offset by strength in both flagship and newer products. Despite one-time pressure on operating margins from elevated marketing spend, management raised guidance for both revenue and adjusted EPS.

1Q26 revenue totaled $24.1bn (+9.9% YoY), exceeding our estimate ($23.9bn) and the FactSet consensus ($23.6bn). Outperformance was driven by robust sales of DARZALEX (+22.5% YoY), TECVAYLI (+33.5% YoY), TREMFYA (+68.3% YoY), and the RYBREVANT/LAZCLUZE combination (+82.7% YoY), delivering the largest upside surprise versus our model. The primary negative variance was a sharp 60% YoY drop in STELARA sales.

Overall, JNJ remains well balanced across Pharmaceuticals and MedTech with a solid competitive position. The launch of ICOTYDE should help bolster the currently softer Immunology segment. In MedTech—particularly the Surgery subsegment—performance will hinge largely on a potential approval of the OTTAVA surgical system later this year.

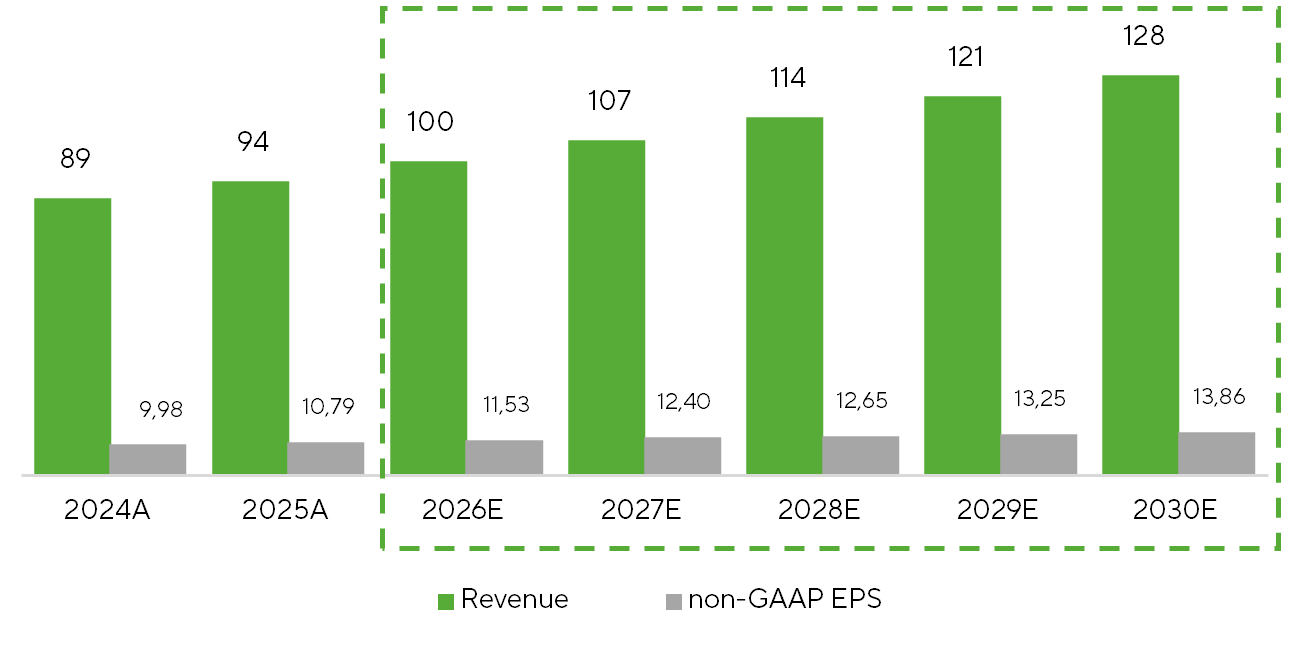

Revenue, $bn, and Adjusted EPS, $, Forecasts

Source: Freedom Broker analysis

Netflix Report

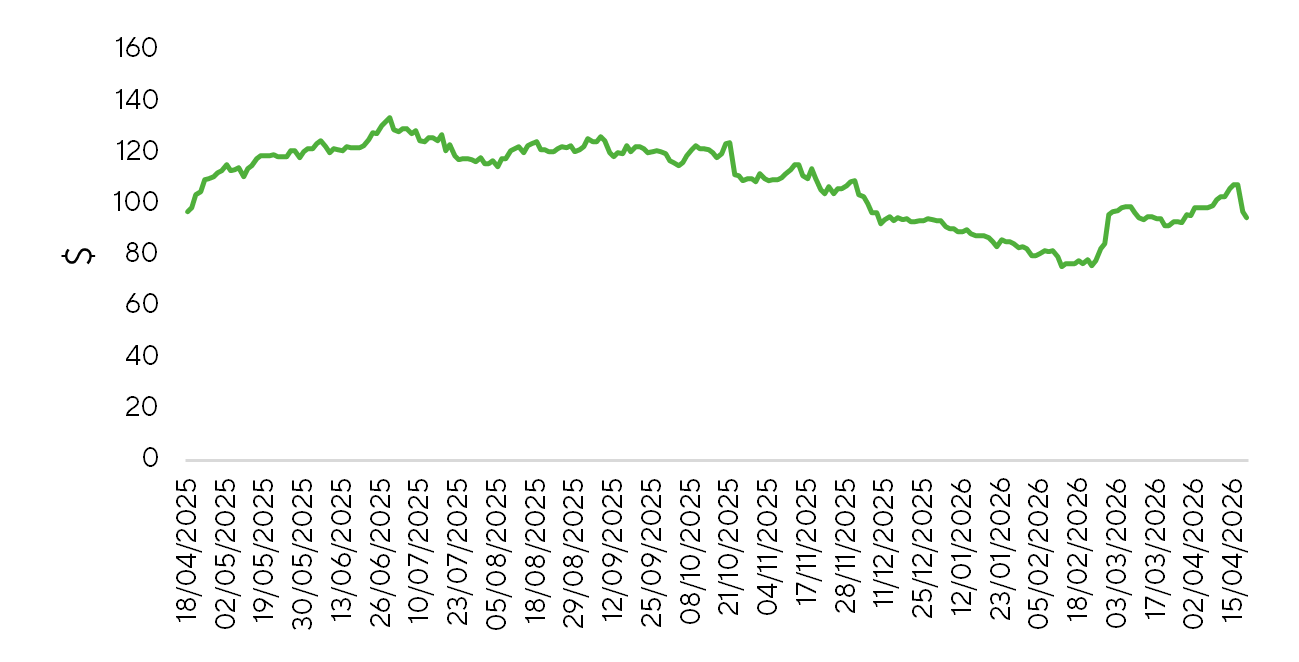

Netflix (NFLX) delivered strong 1Q26 results, beating market consensus across key metrics on the back of robust subscriber additions, pricing actions, growing advertising revenue, and improved retention. The company noted that its internal engagement-quality metric reached a record high in Q1. Reported operating performance also benefited from the recognition of a $2.8bn termination payment related to the canceled Warner Bros. Discovery transaction. However, guidance for 2Q26 came in below preliminary market expectations across all key metrics. Management attributed the softer outlook to content amortization costs being front-loaded in 1H26—peaking in Q2—due to the timing of new releases. The weaker Q2 outlook, coupled with the decision not to raise full-year 2026 guidance, has rekindled concerns about the durability of operating momentum amid ongoing price increases and the need to sustain monetization gains. NFLX shares have already declined more than 12% following the release.

Netfllix Stock Price Trend

Source: FactSet