Investment Review №343. The return of the bulls

The World Bank has spoken out on behalf of consumers

Moderately positive macroeconomic data and World Bank forecasts supported the rise in local stocks

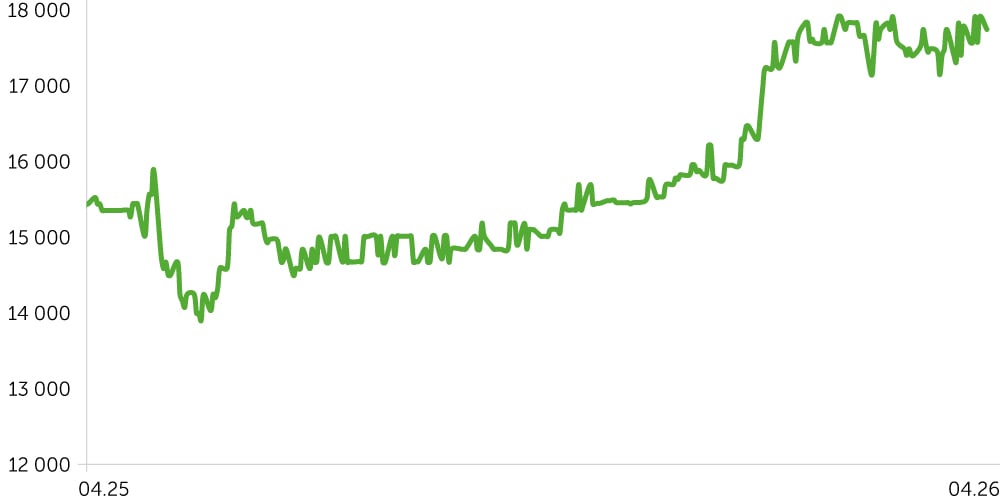

Telecom Armenia Stock Performance (Post-IPO)

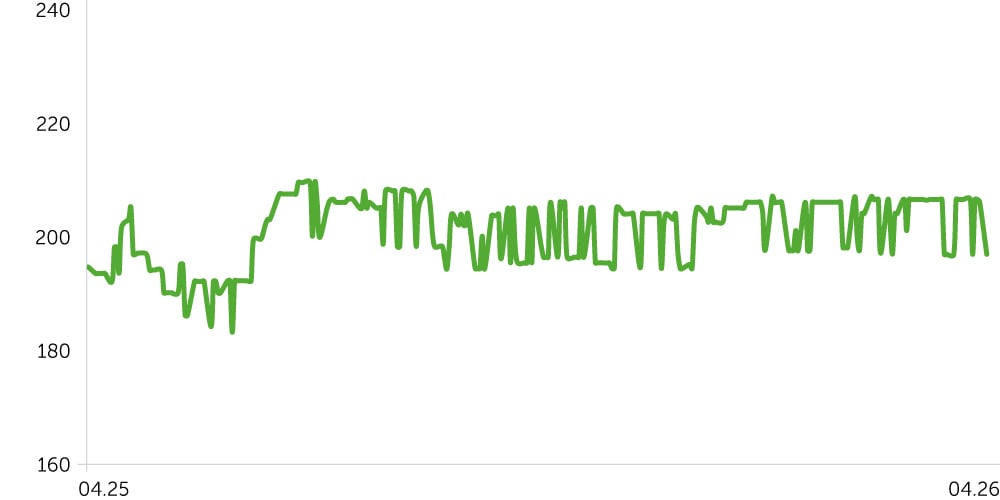

ACBA Bank: 1-Year Stock Trends

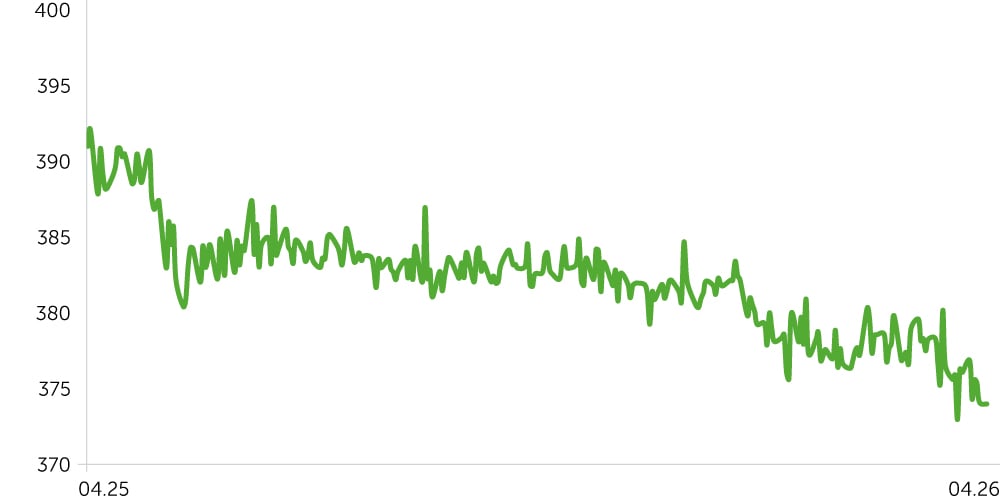

USD/AMD: 1-Year Dynamics

3-Year Corporate Bond Index (AMD) – Post-Update

Between April 6–20, 2026, the Armenian equity market showed selective upside amid improving medium-term macro expectations. Telecom Armenia (AMTL) remained flat despite a modest acceleration in Communication Services revenue growth (vs 2025: +2.7%) to 4.5% YoY in January–February and 6.2% YoY in February. Recent years’ data indicate a constrained growth outlook for the sector (below overall economic growth), which likely continues to weigh on investor appetite for AMTL. ACBA Bank outperformed, rising 2.3% over the period and 18.8% YTD. The move was likely supported by corporate developments, including a new partnership agreement with Interactive Brokers, as well as sustained investor interest in Financials amid a solid domestic macro backdrop. At the macro level, the World Bank revised Armenia’s 2026 GDP growth forecast up to 5.3% (+0.4pp), reinforcing a constructive medium-term outlook. This upgrade—despite expected slowing across the EU and Central Asia—supports the case for continued inflows into Armenian financial assets.

On the fixed income side, the price index of 3Y AMD-denominated corporate bonds remained broadly flat, pointing to a wait-and-see stance among investors amid persistent inflation risks and elevated external uncertainty. At the same time, the World Bank, despite an upgraded GDP growth forecast, points to the region’s vulnerability to external inflationary shocks from the closure of the Strait of Hormuz, as noted earlier. In this environment, the regulator is likely to maintain a cautious stance, with further policy steps dependent on the persistence of inflationary pressures in the near term. Meanwhile, the AMD/USD exchange rate continued to strengthen moderately (+0.4%), reflecting a combination of resilient domestic flows and relatively stable monetary conditions.

Economic Updates

The World Bank raised its GDP growth forecast for Armenia, reinforcing the view of macro resilience despite a broader regional slowdown, while external risks remain elevated. Consumer demand is showing a gradual recovery, while the Communication Services sector posts stable yet subdued growth, primarily supported by telecom operators.

- The World Bank raised its GDP growth forecast for Armenia to 5.3% in 2026 and 5.1% in 2027 (+0.4pp vs January), supported by resilient domestic demand and sustained investment activity. The revision is notable against the backdrop of a slowdown expected in the ECA region to 2.1% and in Russia to 0.8%, highlighting Armenia’s relative macroeconomic resilience. In our view, the upgraded forecast—despite external geopolitical shocks—supports a constructive medium-term outlook and may further underpin investment activity in Armenia.

- Domestic trade in Armenia accelerated to 5.6% YoY and 14.4% MoM in February, bringing January–February growth to 3.3% YoY. The data point to a gradual pickup in consumer activity at the start of the year. Structurally, performance remains uneven: wholesale trade—accounting for 63.5% of total turnover—rose only 0.8% YoY, while retail (32.7% share) posted a stronger 8.1% YoY increase. Auto sales also expanded 5.8% YoY.

- Growth in the Communication Services sector accelerated to 6.2% YoY, despite a slight 1.3% MoM decline. The telecom segment remained the primary driver, posting 6.6% YoY growth, while revenue from TV and broadcasting services increased only 0.1% YoY. As a result, total telecom and media services growth for January–February 2026 stood at 4.5% YoY. Overall dynamics continue to point to subdued structural growth in demand for telecom services and digital infrastructure in recent years.

Corporate News

Team Holding, with Freedom Broker Armenia acting as underwriter, completed the second tranche of its USD bond issuance with a total size of $10m. The notes carry an 8.75% annual coupon, 48-month maturity, quarterly interest payments, and a $100 par value.

Two-Week Outlook

In the period from April 24 to May 4, investor attention will be focused on a combination of updated medium-term forecasts and the release of March macroeconomic data.

Key focus will be the release of March data on CPI, economic activity, and the trade balance. The Producer Price Index (PPI) will also be published, expected to accelerate from 9.5% YoY in February to 10.4% YoY in March. However, market attention will likely remain focused primarily on consumer inflation dynamics. Given CPI previously printed at ~4.5% YoY, investors will assess whether pricing pressures are becoming entrenched. In our base case, a sustained overshoot above the inflation target would strengthen the case for a more hawkish Central Bank stance in the near term. If realized, such a scenario could weigh on domestic fixed-income markets. That said, inflation expectations and their trajectory will also be materially shaped by geopolitical developments. In particular, the closure of the Strait of Hormuz would carry meaningful upside inflation risk for the country, in our view.

Additionally, March data on retail sales and the manufacturing PMI will be released, with a significant slowdown expected in both indicators—from 5.6% to 0.5% YoY and from 23.8% to 15.0% YoY, respectively.