Двухнедельный обзор фондовых рынков №349. Большие надежды

A Race Against GDP

Improved macroeconomic forecasts and rising business activity are reinforcing the bullish trend on the local stock exchange

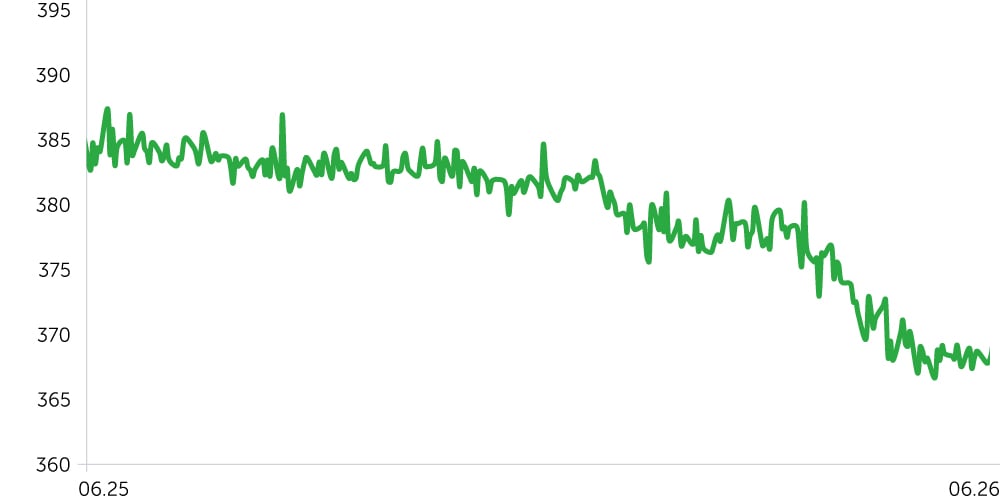

Telecom Armenia Stock Performance (Post-IPO)

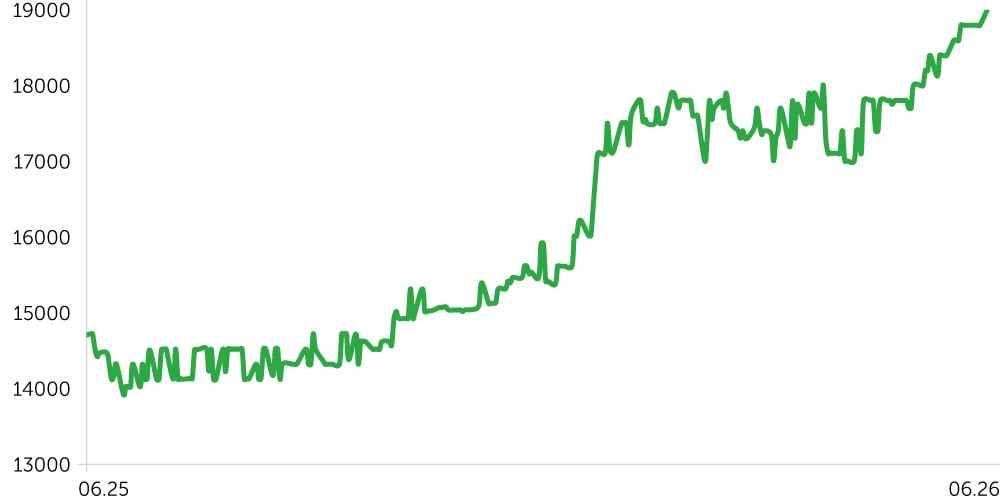

ACBA Bank: 1-Year Stock Trends

USD/AMD: 1-Year Dynamics

3-Year Corporate Bond Index (AMD) – Post-Update

Between June 15 and 29, 2026, the Armenian market continued to firm. Telecom Armenia (AMTL) gained 2.9% over the period and for June overall, while Acba Bank rose 2.2%, bringing its YTD gain to 21.8% and underscoring sustained interest in banks. Sentiment was supported by the Eurasian Development Bank (EDB) raising its 2026 GDP growth forecast to 6.0% and by May’s 11.7% YoY pickup in economic activity, mainly due to construction and services. The growth profile suggests investor appetite for real estate remains strong, weighing on demand for financial assets, and underpins the economy’s relative resilience despite external headwinds.

Debt-market activity remained muted, with the 3-year Corporate Bond Index edging up just 0.1%, reflecting caution amid heightened price-pressure uncertainty. A renewed acceleration in consumer prices could limit the Central Bank’s scope to turn more dovish in H2 and may even prompt renewed tightening. The AMD/USD rate was flat over the period, providing a stabilizing backdrop. However, if restrictions on exports to Russia persist—public sources estimate roughly 10–12% of the country’s total exports are currently restricted—the risk of some dram depreciation increases. That said, ongoing central-bank interventions should continue to partly offset this pressure.

Economic Updates

From June 15 to 29, 2026, the macro data docket was busy. Investors focused on economic activity gauges, the EDB’s forecast, and other releases. The macro tape leaned moderately constructive overall.

- The EDB raised its 2026 GDP growth forecast for Armenia to 6.0% from 5.3%, noting no basis for a downgrade despite Russia’s import restrictions on Armenian goods. It also revised coming-year projections up to 5.7% for 2027 (from 5.3%) and 5.3% for 2028 (from 5.1%). The bank sees momentum supported by a broad set of domestic drivers, reducing sensitivity to idiosyncratic external shocks. In our view, the revision reflects resilient economic activity and some diversification of growth engines, though export dynamics and regional conditions remain key risks to the forecast.

- Armenia’s economic activity accelerated to 11.7% YoY and 9.9% MoM in May 2026, the strongest pace in recent months. Growth was driven by industrial production (+9.5% YoY; +1.2% MoM) and especially construction, which surged 27.1% YoY and 27.2% MoM, underscoring sustained investment momentum. Services (excl. trade) also contributed meaningfully, up 14.7% YoY and 6.9% MoM. By contrast, domestic trade turnover was flat YoY and fell 1.6% MoM, pointing to uneven demand. The May release confirms a rotation in growth and investment drivers toward construction amid more moderate consumer dynamics.

- Producer price inflation accelerated to 9.0% YoY in May 2026 from 7.9% in April, Producer price inflation accelerated. On a month-over-month basis, the PPI rose 1.6% after a 0.7% decline in April, signaling renewed industrial pressures. In our view, the reacceleration in PPI could limit further slowing in consumer inflation in the second half of the year, particularly if construction remains strong and domestic demand stays firm.

Corporate News

- Armenia Moves to Nationalize Electricity Grids: The government has released a draft resolution declaring an overriding public interest in 100% of CJSC Armenian Electricity Grids (AEG). The move is justified by AEG’s strategic role in electricity supply, the need to protect consumers, safeguard energy security, and ensure uninterrupted service. Prime Minister Nikol Pashinyan earlier said the company is already de facto under state control and that the legal transfer will be formalized. In our view, this sets a negative precedent for foreign investors and could weigh on Armenia’s overall investment appeal.

Two-Week Outlook

From July 3 to July 13, the key event is the June CPI release. After May’s slowdown, investors will assess whether disinflation momentum can be sustained amid persistently robust economic activity and a renewed pickup in producer prices. Fundamentals remain solid. The Eurasian Development Bank has raised its 2026 GDP growth forecast to 6.0%, underscoring the resilience of the investment cycle. Construction remains a major growth driver; while supportive in the medium term, it also points to an investment bias toward real estate, adding pressure to domestic financial markets. The services sector is also rebounding, supported by the tourist season. In our view, growth drivers will continue to diversify over the medium to long term, despite Russia’s restrictions on imports of Armenian products.

If, amid a reacceleration in CPI, inflation stays near the top of the target range, room for further monetary easing will be limited. For the debt market, this implies continued caution on the rate trajectory, while the FX market will be sensitive to foreign-trade developments.