Двухнедельный обзор фондовых рынков №349. Большие надежды

Corporate News in Focus of Our Analysts

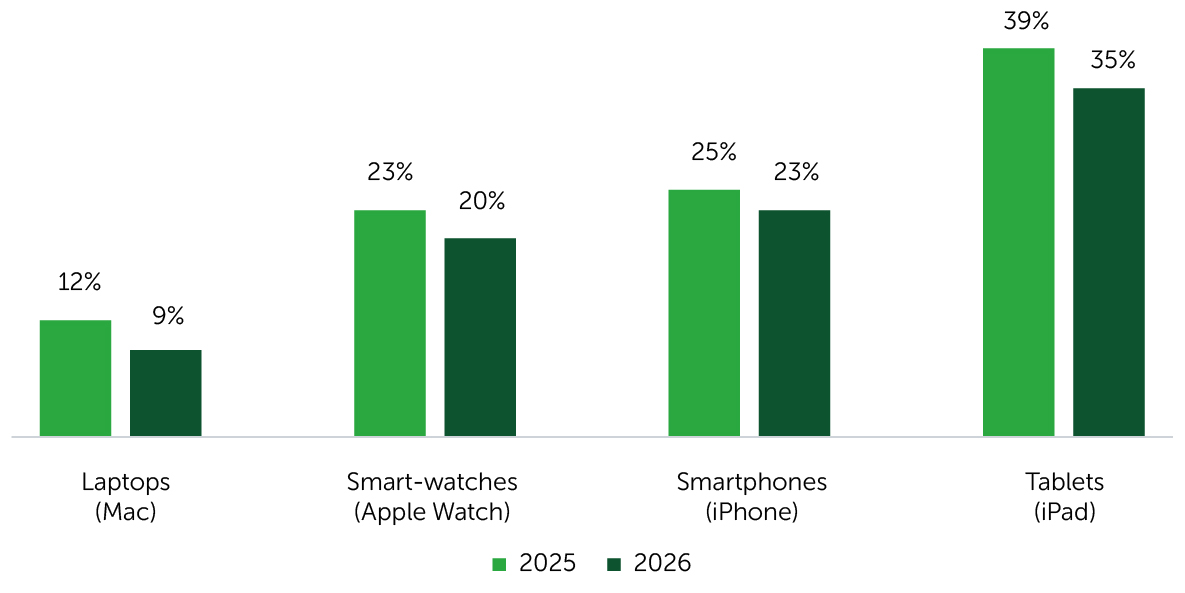

Apple

On June 25, Apple (AAPL) formally passed higher memory-chip costs on to consumers for the first time, raising prices across almost the entire Mac and iPad lineup, as well as Apple TV, HomePod, HomePod mini, and Vision Pro. Prices for iPhone, Apple Watch, and AirPods were left unchanged. Tim Cook also left the door open to further device price increases. Importantly, Apple is moving much more cautiously than competitors, both in timing and product coverage. Rivals have already raised prices by 10–20% and narrowed their lineups toward premium devices. iPhone pricing remains the main uncertainty. Still, investors are increasingly leaning toward the view that next-generation smartphones will be more expensive than previous models. Apple will likely try to soften the blow for customers by increasing minimum flash storage to 256 GB for entry-level models and raising minimum RAM to 12 GB. The need to expand the user base for the new Apple Intelligence-enhanced Siri, also supports higher RAM requirements, as 8 GB of RAM will no longer be sufficient. Despite the price increases, 2026–2027 should still be among Apple’s strongest years for market-share gains across business lines. AAPL shares fell more than 6%, marking the stock’s worst session since April 2025.

Apple’s Global Market Shipment Share by Product, %

Sources: Counterpoint Research, Freedom Broker analysis

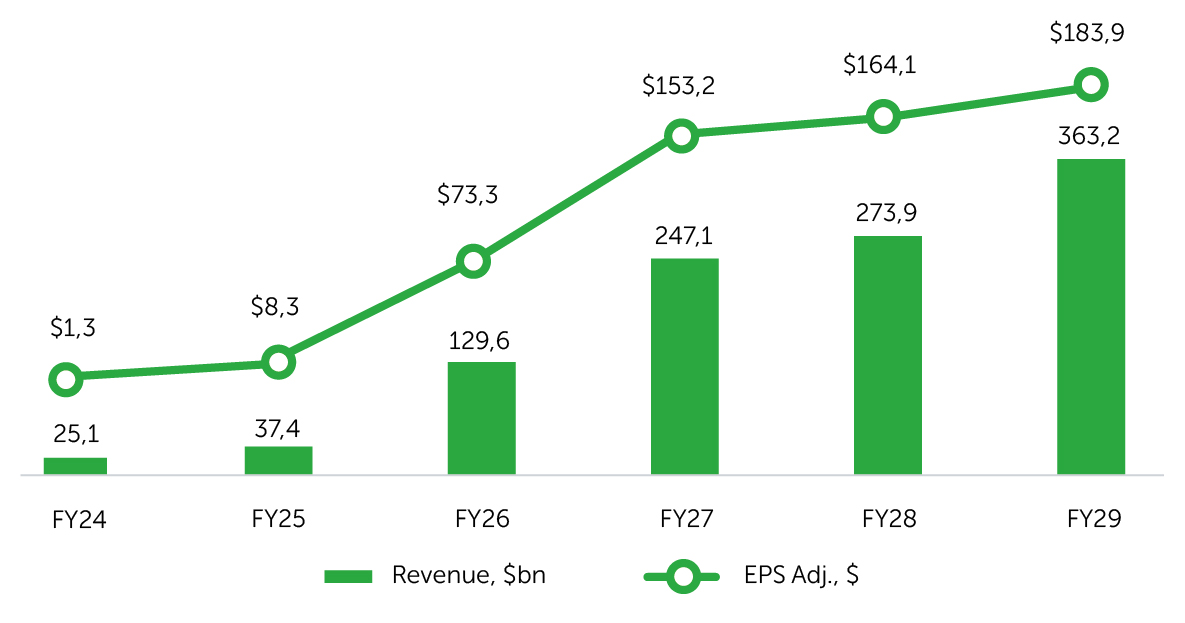

Micron Results

On June 24, Micron Technology (MU) reported quarterly results, delivering a record quarter driven by pricing rather than volumes. An acute structural shortage in DRAM and NAND, with demand running well ahead of supply constrained by process-node economics, HBM’s wafer appetite, and multi-year fab lead times, drove record revenue, profitability, and exceptional cash flow across all four segments. More importantly, Micron is undergoing a structural shift. The company is moving a significant share of volumes into multi-year strategic customer agreements, or SCAs, with take-or-pay provisions that lock in both volume and pricing parameters. According to management, even at the minimum permitted pricing levels, margins would exceed the peaks of prior cycles. If long-term contracts become the new reality for the business, they could transform Micron’s traditionally cyclical model into a higher-margin and more predictable one, supporting higher capex and a higher valuation multiple for the stock. The market took an optimistic view of this business-model shift, although the new contract structure does limit upside potential. More importantly, however, it provides protection against price declines and demand weakness. MU shares closed up 15.7% on June 25.

Key Financials of Micron Technology, Inc. (MU)

Sources: FactSet, Oracle, Freedom Broker

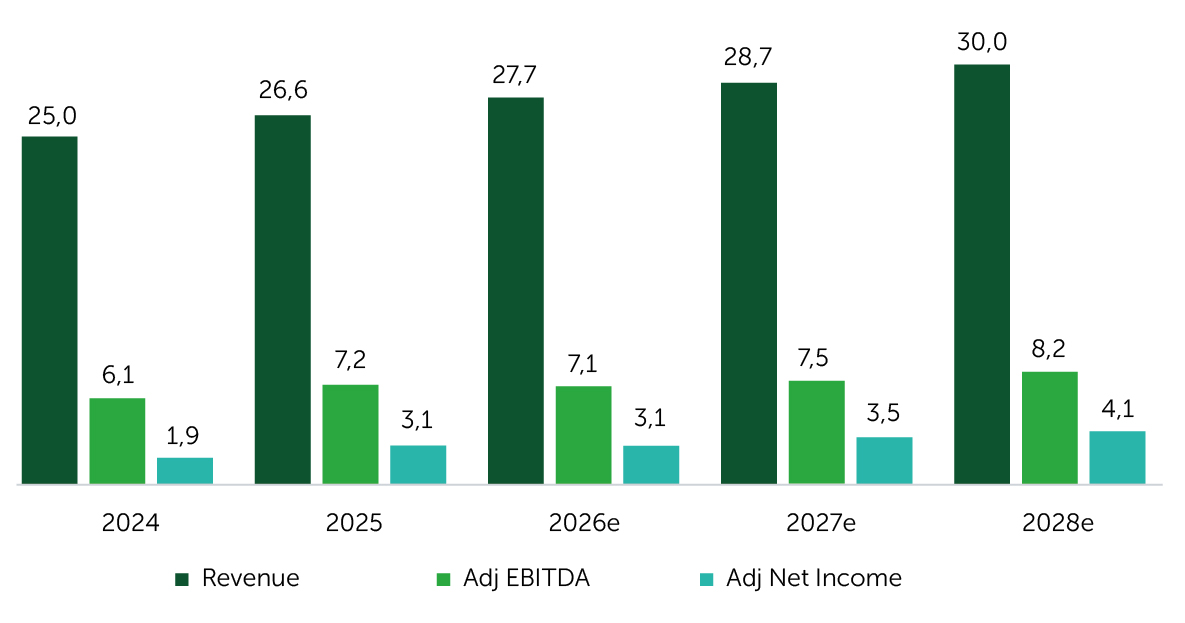

Carnival Results

On June 23, Carnival Corp. (CCL) reported fiscal Q2’26 (ended May 31) results that topped earnings expectations while revenue was in line. Adjusted EPS stood at $0.41 versus $0.34 consensus, adjusted EBITDA reached a record $1,582m, and revenue amounted to $6,663m. Adjusted net income rose more than 20% YoY to $569m despite nearly 30% higher fuel prices. More important than the size of the beat was its composition: upside was driven by tighter cost control and fuel efficiency, while overall demand was in line with expectations. Unit costs ex fuel, in constant currency, were flat year over year—about 250 bps better than March’s guidance. Customer deposits hit a record $9.0bn. CCL shares declined by about 6% on June 23, reflecting a cut to the full-year net yield outlook rather than the quarterly print. The investment case hinges on a simple dynamic: net yields must outpace ex-fuel unit costs. Q2 results confirmed this, but with a near-term pivot to cost control, the expected acceleration in yields has been deferred toward 2027. Management lowered its FY26 net yield target in constant currency from ~2.75% to ~1.75%, citing localized demand softness on certain European and Mediterranean itineraries linked to the conflict in the Middle East. We view the sell-off as overdone: the company is 93% contracted for 2026 at historically high prices, and 2027 bookings are ahead of last year. Fuel remains a source of upside optionality: any decline in oil prices would expand margins further.

Key Financial Metrics — Carnival Corp. (CCL), $bn

Sources: Carnival, Freedom Broker

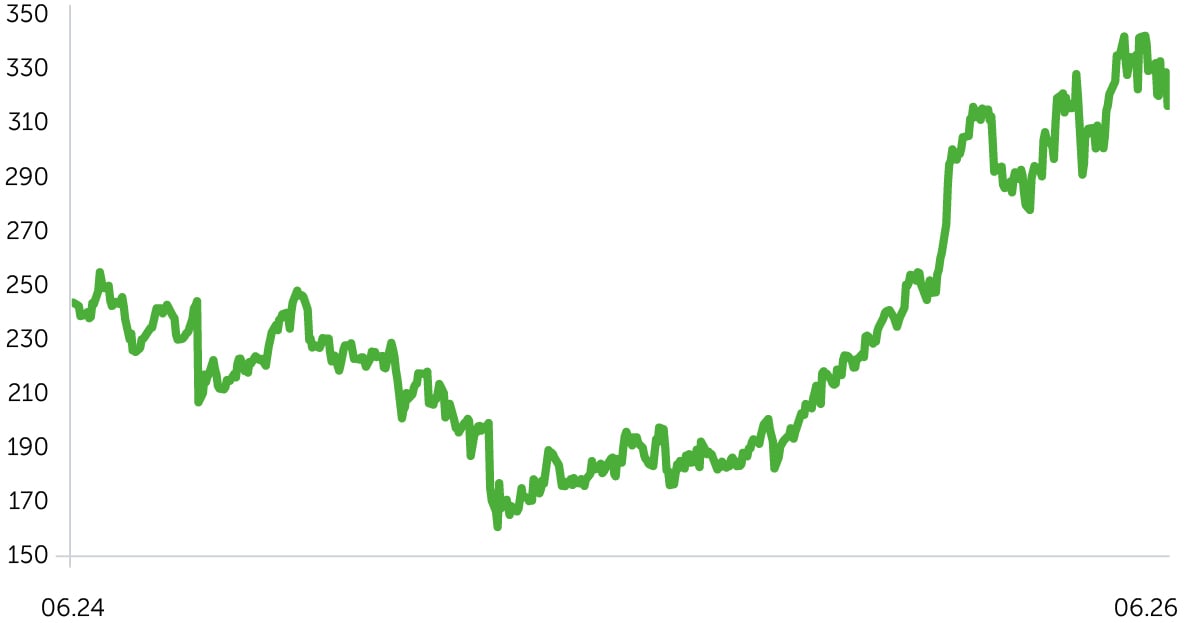

FedEx

FedEx delivered a strong fiscal Q4’26, beating EPS estimates due to double-digit revenue growth. Outperformance was led by the Express segment, with volume growth in the U.S. and international export markets, alongside higher yield per package. Management underscored a shift toward higher-margin B2B and premium B2C customers while pruning low-margin economy delivery services. The Network 2.0 program materially reduced structural costs and kept capital intensity at historic lows. Record FCF supported a dividend increase and authorization of up to $1bn in share repurchases. During the reporting period, FedEx completed the spin-off of FedEx Freight into a standalone, publicly traded company, strengthening the balance sheet and sharpening the focus on margin and profit growth.

FedEx Stock Performance

Source: FactSet

Fed Bank Stress Test

The Fed’s annual stress test showed all 32 participating banks maintained capital above required minimums even under a severe global recession scenario. Assumptions included the unemployment rate rising to 10%, a 4.6% GDP contraction, a 58% equity-market decline, a 30% drop in home prices, and a 39% decrease in commercial real estate values. Estimated losses on loans and other exposures totaled $708bn. The aggregate CET1 ratio dropped from 12.8% to an 11.2% trough before rebounding to 12.7% by the end of the nine-quarter horizon. The 1.6 pp pullback was smaller than last year’s 1.8 pp, though the comparison is not clean given the sample expansion from 22 to 32 banks.

Under a stress scenario, capital was further pressured by roughly 10% growth in loan balances in 2025, tougher assumptions on commercial real estate and corporate spreads, as well as lower estimated income from AFS portfolios. These headwinds were more than offset by higher projected net interest income, reflecting improved bank performance and a higher rate path.

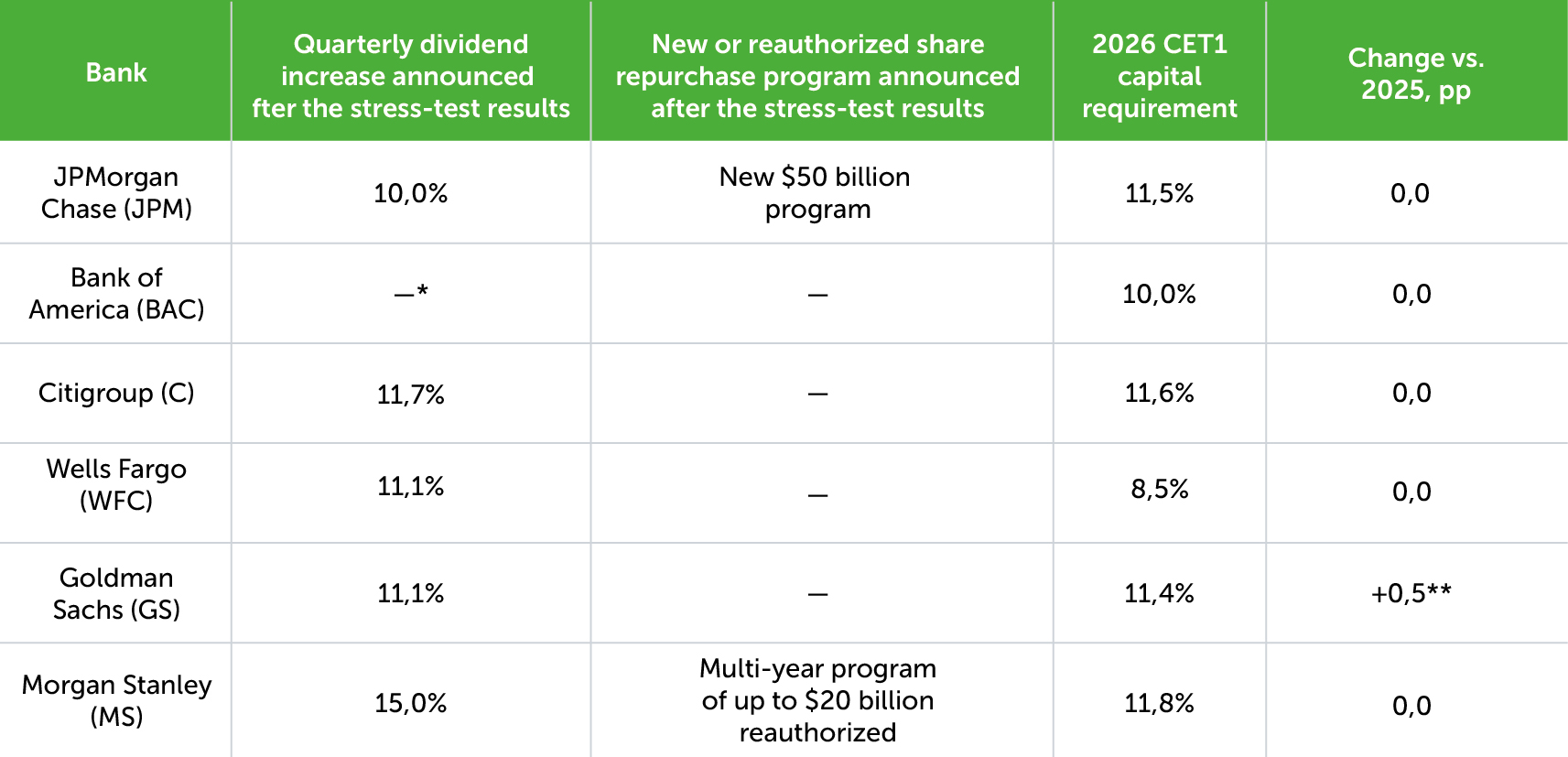

Initially, a revision of stress capital buffers subject to 2026-cycle results was not expected: back in February, the Fed indicated current SCBs would be maintained through 2027. The next update is anticipated after the 2027 stress test, using refined models that incorporate public feedback. Following the earnings releases, JPMorgan, Citigroup, Wells Fargo, Goldman Sachs, and Morgan Stanley announced dividend increases; JPMorgan and Morgan Stanley also announced new or reauthorized share buybacks.

Largest U.S. Banks – Key Metrics

Source: Federal Reserve, bank data, Freedom Broker analysis

* Bank of America will determine the quarterly dividend amount at its July 2026 Board meeting.

** The total CET1 requirement for GS rose by 50 bps, driven by an increase in the G-SIB surcharge to 3.5% from 3.0%, effective January 1, 2026. The bank’s SCB remains 3.4%; this change is unrelated to the stress-test results for 2026.