Financier №2 (42) 2026

Prudent Investments

Freedom Broker Analysts Offer Stocks Of Companies From Various Economic Sectors To Diversify Your Portfolio

Upsides and quotes are presented as of April 22, 2026

Mikhail Denislamov,

Deputy Director, Analytical Department, Freedom Finance Global

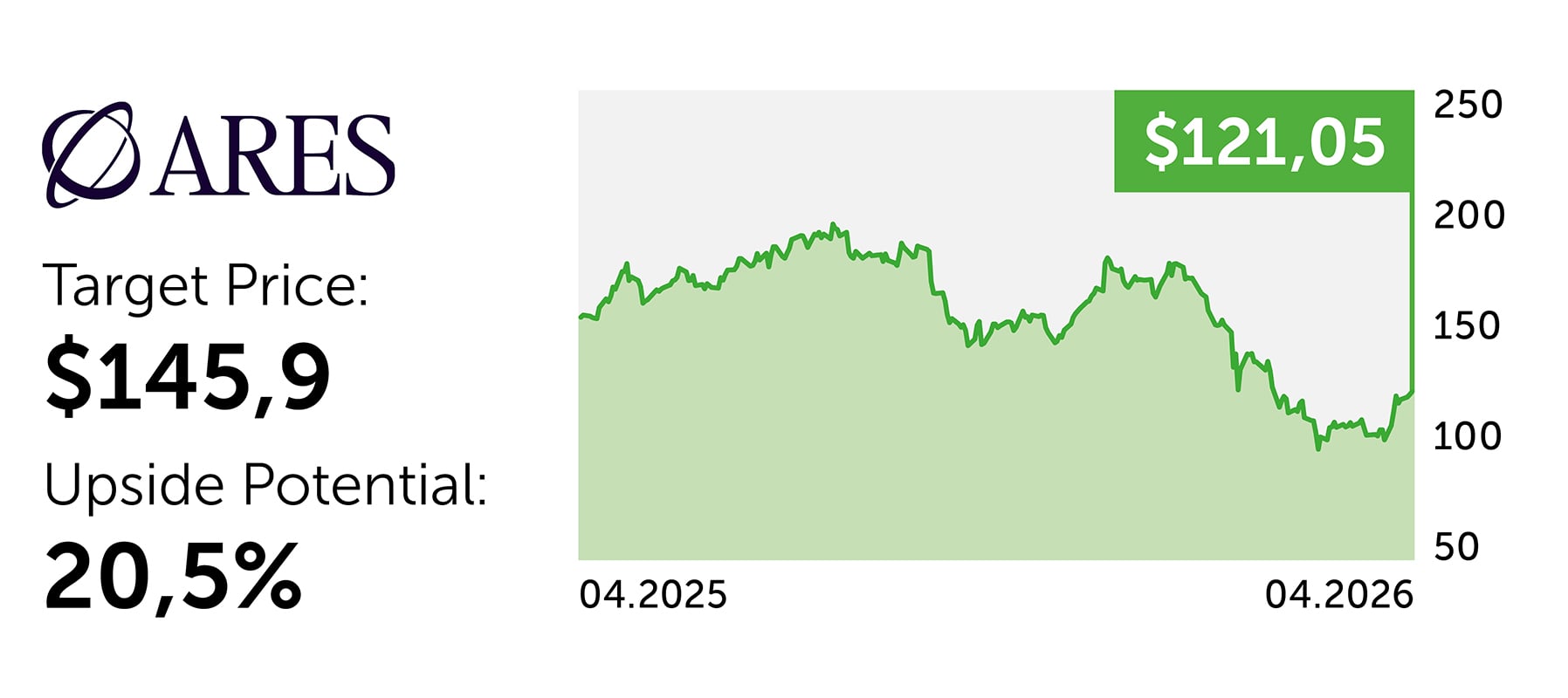

Ares Management (ARES) is growing amid rising risk assessments for private lending, which are not systemic for the company. Its diversified platform continues to successfully attract capital. At the end of 2025, assets under management amounted to nearly $623 billion, and available capital exceeded $150 billion. This creates opportunities for new transactions and an expanded fee base. Management forecasts that the fundraising segment will break its 2025 record this year. If market sentiment toward private lending normalizes, Ares could benefit from higher valuation multiples.

Brookfield Asset Management (BAM) focuses on infrastructure, energy, physical assets, and private businesses. A significant portion of capital is raised for the long term or in perpetuity, making the company's cash flows predictable. The volume of fee-generating funds reached $603 billion in 2025, fundraising generated $112 billion, and fee and commission income grew by 22%. Among the positive drivers are new flagship funds, one of which Brookfield has already raised $5 billion against a target of $10 billion. For investors, the issuer's attractiveness is linked to a steady increase in fee and commission income.

Ameriprise Financial (AMP) is benefiting from demand for financial planning, growing fee-generating assets, and strong client engagement. In Q1, operating EPS reached $11.26, with total assets under management reaching approximately $1.7 trillion. Core business margins remain at 30%. An additional growth driver was a partnership with Huntington National Bank, which is expected to bring approximately 260 financial advisors and nearly $28 billion in client assets to the platform. AMP shares are attractive due to their predictability, high profitability, and defensive profile.

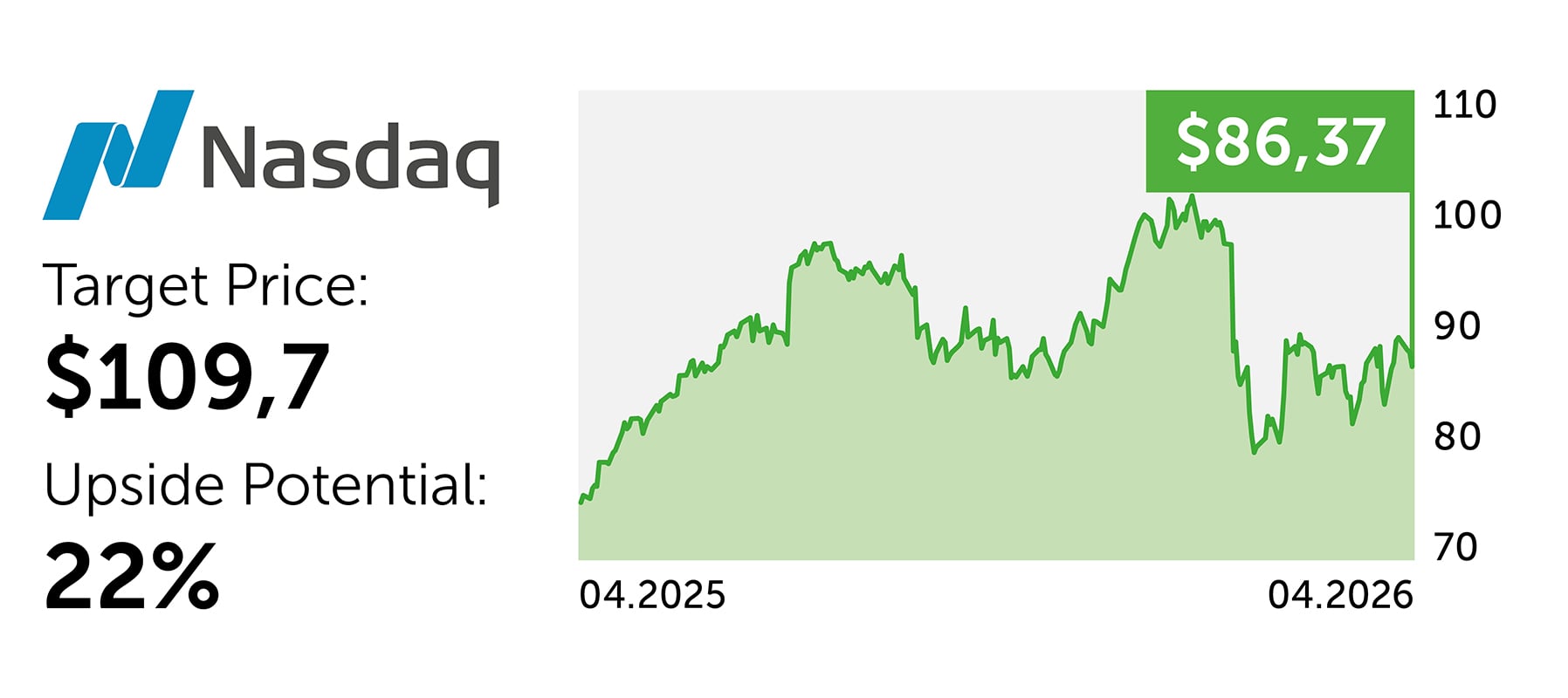

NASDAQ (NDAQ) has maintained its profitability through a focus on financial technology, big data, and risk management software solutions. In Q1, net income grew 14%, with ARR reaching $3.2 billion, and FinTech revenue up 20%. Positive drivers include a recovery in the IPO market and the growth of the index business, which is benefiting from demand for passive and thematic products. NDAQ shares are attractive due to a combination of sustained growth in subscription revenue, high free cash flow, and moderate support from market volatility.

Yerlan Abdikarimov,

Director of the Financial Analysis Department, Freedom Broker

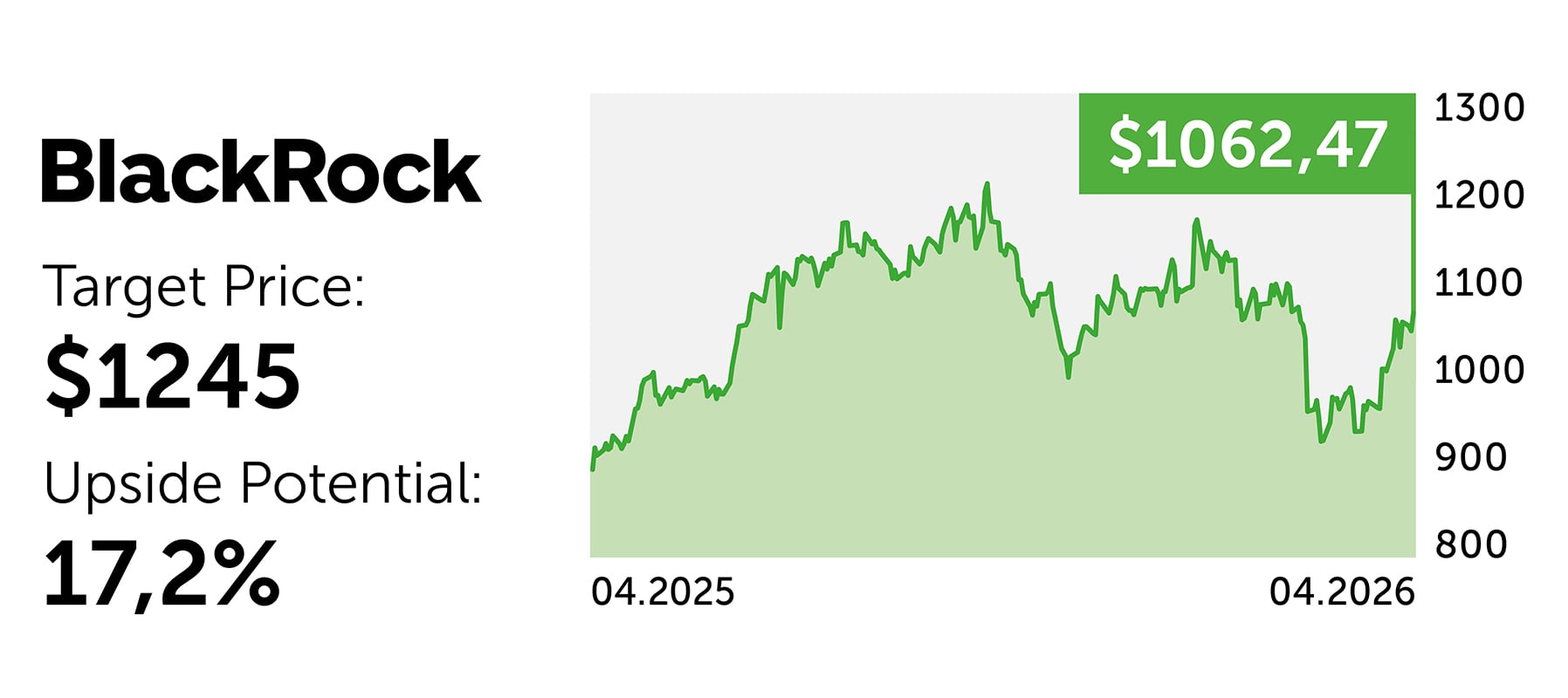

BlackRock (BLK) reported a 27% YoY increase in revenue in Q1, reaching $6.69 billion. Adjusted EPS reached $12.53 billion, net cash inflows totalled $130 billion, and organic core fees grew 8%. Operating margin increased to 44%. Driven by the iShares ETF, private markets, and Aladdin segments, as well as subscription services, BlackRock (BLK) reported a 10% increase in buybacks during the quarter. The fund manages $13.89 trillion in assets under management (AUM). Despite fee pressure, volatility, and exposure to the private lending market, the current valuation is attractive for long-term investments.

Blackstone (BX) demonstrates strong fundamentals, and its 15% decline since the beginning of the year is due to the market's overvalued risks in alternative investments. Fees and commissions will continue to grow, driven by private lending, insurance solutions, multi-strategy investments, and real estate. Concerns about private lending are exaggerated, as institutional investors maintain long-term liabilities and there are no signs of a systemic crisis. An additional growth driver will be the expanded access of alternative investments to 401(k) retirement plans in the US, which will provide the fund with new inflows.

Brookfield Corporation (BN) forecasts average annual profit growth of more than 20% through 2030. This growth will be driven by its fee-based asset management business and the Wealth Solutions insurance platform, with approximately $143 billion in assets. The company estimates its profit will grow 34% annually. Supporting factors include the recovery of the global real estate market, investments in AI infrastructure (the market is estimated to be worth $7 trillion over the next decade), and the availability of $160 billion in capital for new deals. BN shares are trading significantly below the company's internal valuation. The upside is achieved through an increase in capital and dividends.

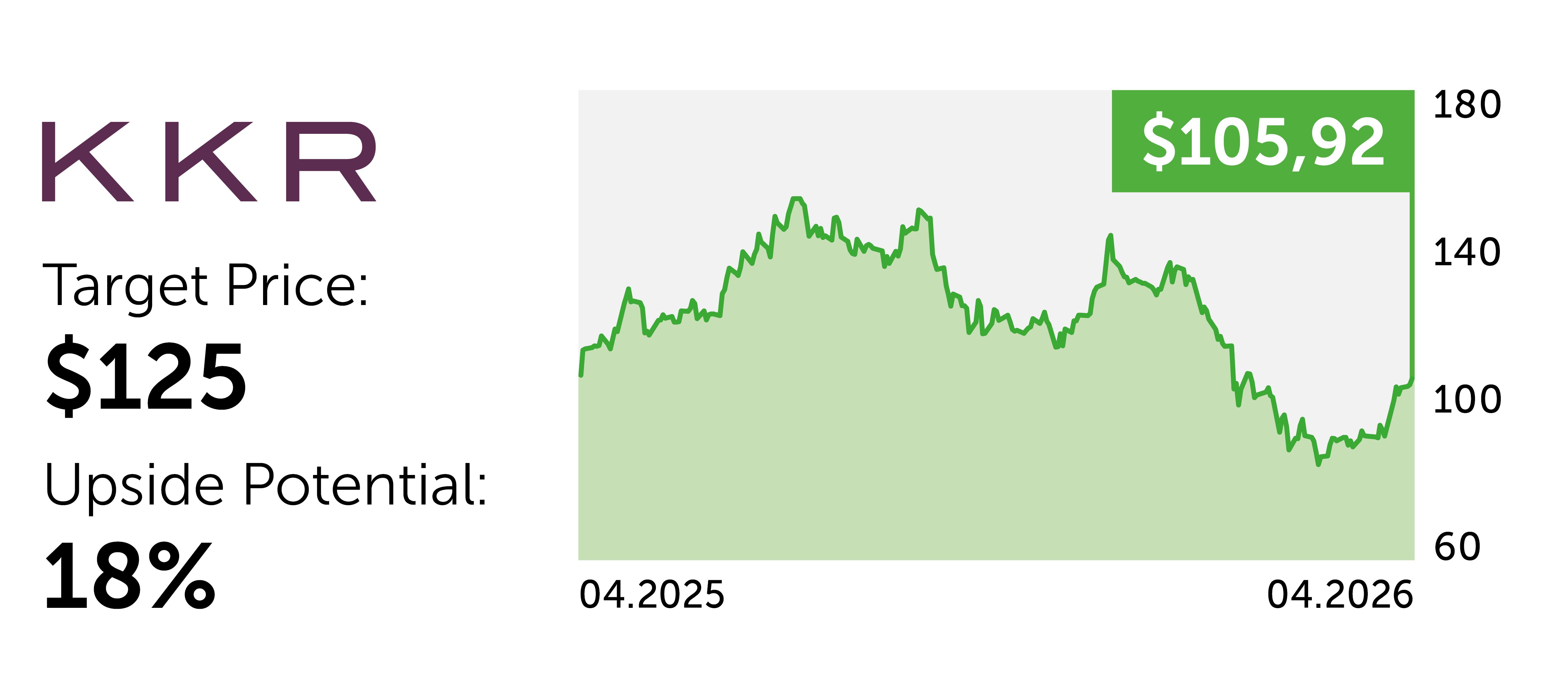

KKR & Co. (KKR) is successfully diversifying its revenue sources. Integration with Global Atlantic has strengthened its internal "capital cycle," whereby insurance assets generate a reserve of funds for investment. Assets under management, which generates commissions, are growing. In 2025, KKR raised a record $129 billion in new capital, and total portfolio implied unrealized gains reached $19 billion. Retail investor channels are rapidly expanding. The EPS guidance for the current year is $7. The company regularly increases its dividend, and its current valuation appears justified due to the dynamic operating performance.