Financier №2 (42) 2026

Sergey Glinyanov

Senior Analyst Freedom Finance Global

The Architecture of Trust

Why Wall Street Remains the Global Financial Hub Despite All Crises

As of early 2026, the total capitalisation of the US stock market has reached $69 trillion - about half the value of all public companies globally. For comparison, EU countries account for less than 12% and China for around 10%. This gap is explained not only by the size of the economy but also by the enormous level of trust in the market from investors worldwide.

This trust is not an abstract concept but a set of specific institutions, laws, and mechanisms. They guarantee investors that their money will not disappear due to a broker’s bankruptcy, a company will not falsify reports with impunity, or their pension will not vanish when changing employers.

These institutions were not acquired for free. Their emergence in the US is the result of learning from mistakes the authorities made after every financial crisis.

In this article, we will discuss the seven pillars on which Wall Street stands today.

Before the Foundation

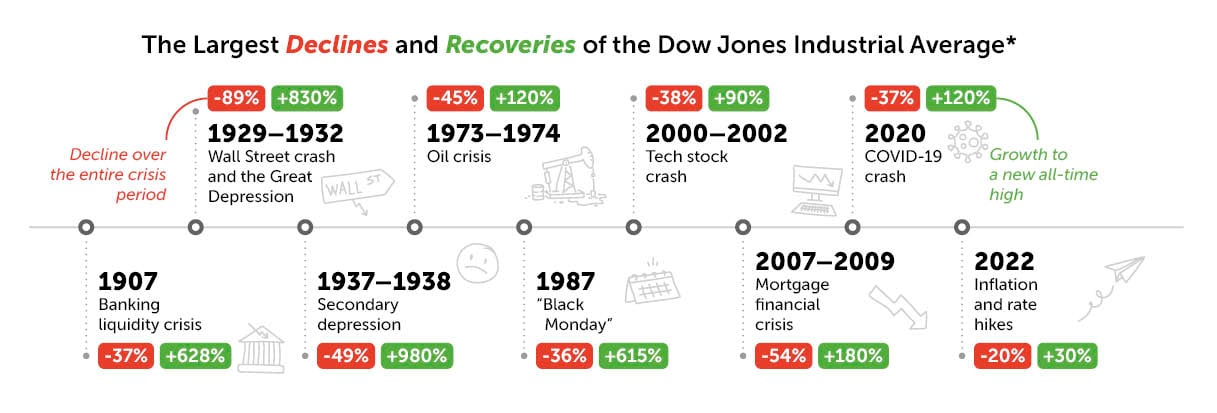

Stock exchanges emerged in America at the end of the 18th century, but until the early 20th century, the stock market operated without unified “rules of the game” in their modern sense. Key transformations in both US markets and the oversight system occurred in the 20th century - and they remain in effect today. The trigger for these changes was the 1907 panic, which caused the stock market to fall by almost 50%. The legendary financier and founder of J.P. Morgan, John Pierpont Morgan, was the only person who managed to coordinate a “rescue operation” at that time. He gathered a group of major bankers, locked them in the library of his mansion, and did not let them out until they agreed to invest in market stabilisation.

A system dependent on the goodwill of one person clearly could not function for long. Six years later, the US Congress made a decision that would change everything.

The Federal Reserve System (1913)

In December 1913, Congress established the Federal Reserve System (Fed) - the central bank the United States had refused to create for the previous 120 years. Initially conceived as a technical tool to regulate the money supply and provide liquidity to banks during crises, the Fed’s role as a systemic stabiliser was fully established only after the crises of 1929 and 2008.

The emergence of a “lender of last resort” independent of private interests became critical for enhancing the system’s stability.

Bank Guarantees and Fair Offering (1933)

In 1929, the Dow Jones Industrial Average (DJIA) fell by almost 90 % from its historical highs. Thousands of banks went bankrupt, taking with them the savings of millions of families.

In response to the crisis and the Great Depression, two fundamental laws were introduced in 1933: The Glass‑Steagall Act, which separated commercial and investment banks. The logic was simple: a bank holding private individuals’ money should not use those funds for stock trading. This act also established the Federal Deposit Insurance Corporation (FDIC), which guaranteed the safety of bank deposits in case of a financial institution’s bankruptcy.

The Securities Act of 1933, which set rules for initial public offerings (IPOs). Since then, companies entering the market have been required to provide investors with complete and accurate information about themselves.

A Transparent Secondary Market (1934)

In 1934, Congress passed the Securities Exchange Act, establishing the Securities and Exchange Commission (SEC). The new body monitored issuers’ reporting and information disclosure, fought insider trading, and oversaw exchanges and brokers.

Then-US President Franklin D. Roosevelt appointed Joseph Kennedy Sr., a man who had personally engaged in market manipulation in the 1920s, as the first chairman of the new regulatory agency. Thus, the father of the future legendary President John F. Kennedy managed to establish the SEC's operations.

Unlike Europe, the United States ultimately opted for transparency and uniform disclosure standards rather than direct state control over the market.

Source: Yahoo.Finance

*The Dow Jones Industrial Average (DJIA) is one of the oldest stock indexes, reflecting the performance of shares in 30 of the largest US public companies.

Protection of Broker Clients (1970)

By the mid‑20th century, the stock market had grown so much that a new class of risks emerged - not from issuer fraud but from the potential bankruptcy of intermediaries. Until 1970, the collapse of a brokerage firm meant a complete loss of assets for clients. To protect them, Congress created the Securities Investor Protection Corporation (SIPC). Now, brokerage accounts up to $500 000 are state‑insured.

Pension Funds (1974–1981)

In 1974, lawmakers passed the Employee Retirement Income Security Act (ERISA), introducing special 401(k) accounts with tax incentives. Employers shifted from fixed‑payout pensions to defined‑contribution plans, allowing employees to choose their investments — mostly in stock and bond funds.

As a result of the reform, the majority of middle-class Americans became co-owners of public companies by the 2000s, creating constant institutional demand on the market — a scale unseen in any other country. Today, $8 trillion in exchange‑traded assets are held in 401(k) pension accounts.

Lessons of Fraud (2002)

A series of early‑2000s corporate scandals exposed a fundamental flaw: existing regulation did not protect investors from systematically misleading financial statements. The issue came to light after the bankruptcy of Enron (peak capitalisation: $63 billion). Investigators discovered that the company had been concealing losses for years through a network of off-balance sheet structures. Enron was followed by telecom provider WorldCom, which alleged $11 billion in accounting fraud, and its auditor, Arthur Andersen (one of the top 5 accounting firms in the US).

In response, Congress passed the Sarbanes‑Oxley Act (SOX) in 2002, tightening requirements for corporate reporting and increasing the personal liability of management. Since then, CEOs and CFOs of public companies must personally sign off on financial releases.

Test of Strength (2008–2010)

The 2008 collapse of the real estate bubble and mortgage‑backed securities led to the bankruptcy of Bear Stearns and Lehman Brothers, causing investors to lose trillions of dollars. The market crash revealed gaps in over‑the‑counter (OTC) derivatives regulation — the “bottom of the iceberg” of total losses.

In 2010, US authorities passed the Dodd‑Frank Act, launching the most comprehensive reform since the Great Depression. As a result, the Financial Stability Oversight Council and the Consumer Financial Protection Bureau were established, the Federal Reserve received expanded powers to regulate the systemically important institutions, and professional participants were required to trade standardized derivatives through clearinghouses.

Trust as a Competitive Advantage

The US financial system was not designed as a single entity. It evolved gradually, learning from crises and improving control mechanisms and protections for market participants. As long as this adaptability continues, the American market will remain the primary “home” for global capital.